Over the Week 17, MABUX Bunker Index showed a slight downward correction

The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

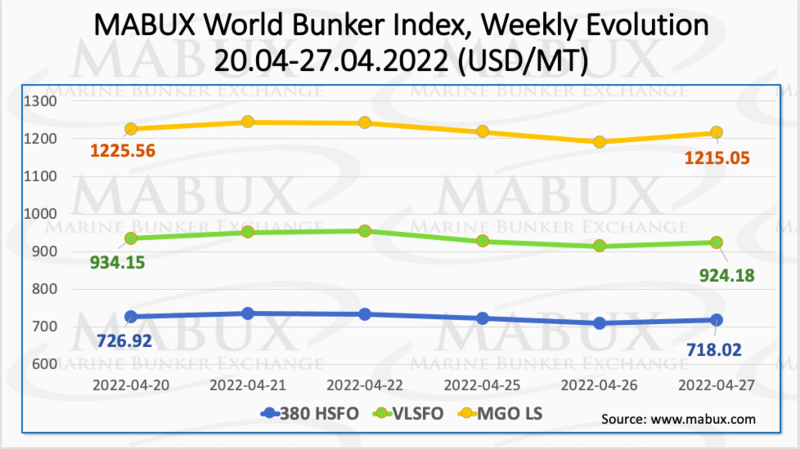

Volatility in the global bunker market, caused by the military conflict in Ukraine, is gradually decreasing, and bunker prices are in a state of temporary stabilization. As a result, over the Week 17, MABUX Bunker Index showed a slight downward correction. The 380 HSFO index fell by 8.90 USD: from 726.92 USD/MT to 718.02 USD/MT. The VLSFO index went down by 9.97 USD: from 934.15 USD/MT to 924.18 USD/MT. The MGO index also dipped by 10.51 USD (from 1225.56 USD/MT to 1215.05 USD/MT). At the same time, high volatility continues to persist in the market.

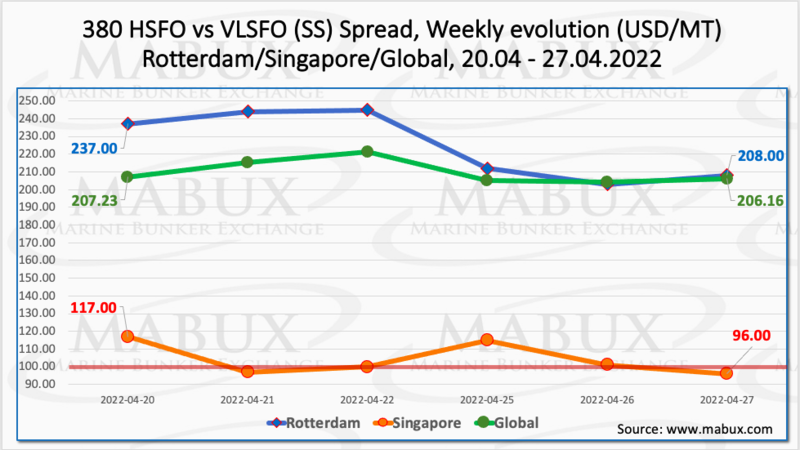

The Global Scrubber Spread (SS) weekly average - the price difference between 380 HSFO and VLSFO - continued its moderate decline over the week - minus $1.99 ($209.92 vs. $211.91 last week). In Rotterdam, the average value of SS Spread, on the contrary, rose from $220.83 to $224.83 (plus $4.00 compared to last week). At the same time, 380 HSFO/VLSFO price difference at the Port of Singapore continues to narrow: the average down by another $19.17 (from $123.50 to $104.33), and in absolute value, SS Spread fell below the $ 100 psychological mark and showed $ 96 as of April 27. More information is available in the Price Differences section of mabux.com.

Benchmark prices for natural gas in Europe rose sharply as Russian gas monopoly Gazprom confirmed that it has stopped supplies to Poland and Bulgaria. The EU and Russia are still in a standoff over demand that Russia’s “unfriendly” nations—such as all EU members and the UK, among many others—pay in rubles for Russian gas. Meanwhile, the European Commission said that companies in the EU may have a way to pay for Russia’s gas in rubles without violating sanctions on Moscow. Due to high volatility in European gas market LNG as a bunker fuel is still not listed.

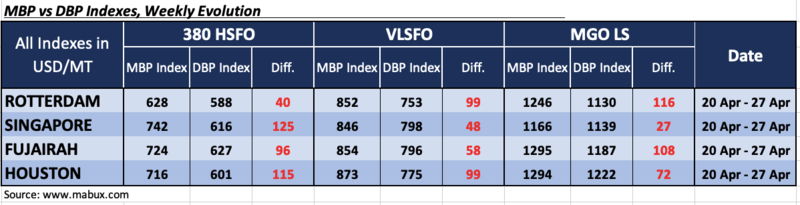

Over the Week 17, the average correlation trend of MABUX MBP Index (market bunker prices) vs MABUX DBP Index (MABUX digital bunker benchmark) did not change: all major bunker fuels are in the overcharge zone in all selected ports. Thus, 380 HSFO fuel’s overcharge margins in a week were: in Rotterdam - plus $ 40 (plus $ 33 last week), in Singapore - plus $ 125 (plus $ 107), in Fujairah - plus $ 96 (plus $ 97) and in Houston - plus $115 (plus $92). MABUX MBP/DBP Index (MBI) overprice premium in the 380 HSFO segment rose slightly.

VLSFO fuel grade, according to MBI, was also overpriced at all selected ports: plus $99 (plus $82) in Rotterdam, plus $48 (plus $44) in Singapore, plus $58 (plus $47) in Fujairah, and plus $99 (plus $102) in Houston. MBI did not have a firm trend in the VLSFO segment: the overpricing increased in Rotterdam, Singapore and Fujairah, but decreased in Houston.

As for MGO LS, MBI also registered an overpricing of this type of fuel over the week in all four selected ports in a week: Rotterdam - plus $116 (plus $84 a week earlier), Singapore - plus $27 (minus $37), Fujairah - plus $108 (plus $101) and Houston - plus $72 (plus $119). Here, MBI also did not have a firm dynamics and changed irregular: growth in Rotterdam and Fujairah, decline in Singapore and Houston.

The Port of Rotterdam has reported that its freight throughput for the first quarter of 2022 was 1.5% down y-o-y, with a big drop in mineral oil products and Russian fuel oil cargoes in particular. In total, liquid bulk throughput decreased by 1.0% to 51.5 million tonnes. While the volume of crude oil remained virtually unchanged (just 0.2% down at 25.5 million tonnes), the throughput of mineral oil products – and fuel oil in particular – was down significantly, dropping more than 20% at 13.5 million tonnes. The Port Authority noted that around 13% of Rotterdam’s cargo throughput in 2021 was ‘Russia-oriented’ – and roughly 30% of crude oil, 25% of LNG, and 20% of oil products and coal came from Russia. While Rotterdam’s Q1 results registered a drop in the throughput of Russian cargoes, the full impact of the Russia-Ukraine conflict will be more apparent in the Q2 figures.

The global bunker market remains highly volatile amid the ongoing military conflict in Ukraine. We expect bunker indices to edge up next week.

By Sergey Ivanov, Director, MABUX

All news