The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

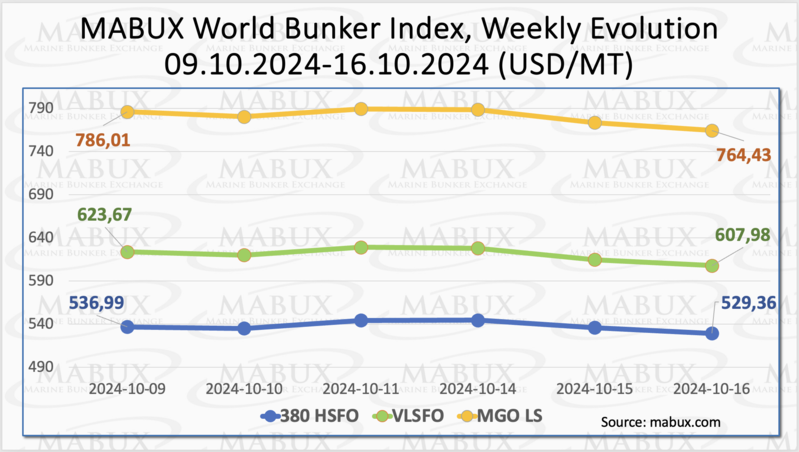

In Week 42, the MABUX global bunker indices experienced a general decline. The 380 HSFO index fell by USD 7.63, moving from USD 536.99/MT last week to USD 529.36/MT. The VLSFO index decreased by USD 15.69 (USD 607.98/MT versus USD 623.67/MT last week). Similarly, the MGO index declined by USD 21.58 (from USD 786.01/MT last week to USD 764.43/MT). However, as of the time of writing, a moderate upward correction was observed in the global bunker market

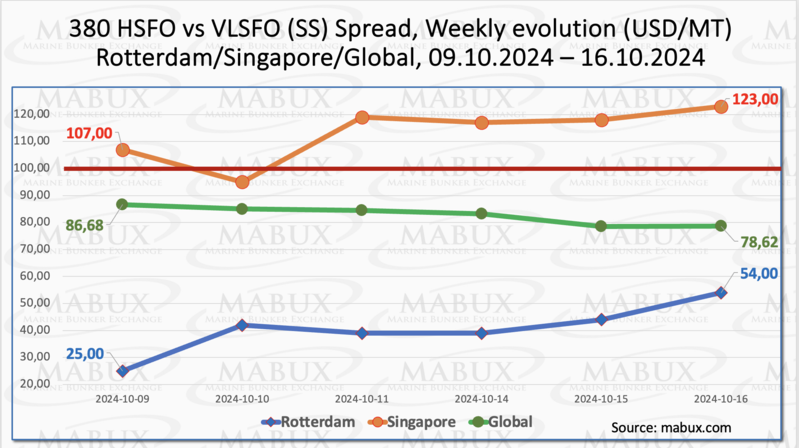

MABUX Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - continued to decline, dropping by $8.06 (from $86.68 last week to $78.62), remaining steadily below the $100 breakeven mark. Meantime, the weekly average decreased by $4.86. In Rotterdam, SS Spread saw a moderate growth of $29.00 ($54.00 versus $25.00 last week), though the weekly average fell by $5.17. In Singapore, the price gap between 380 HSFO and VLSFO widened by $16.00: from $107.00 last week to $123.00, surpassing the $100 mark midweek. Despite this, the weekly average in Singapore narrowed by a marginal USD 0.83. Irregular fluctuations continue to dominate the SS Spread dynamics, and we anticipate no clear trend in the coming week. More information is available in the Differentials section of mabux.com.

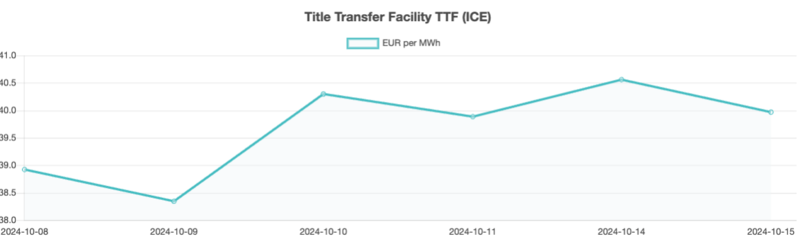

The International Energy Agency (IEA) has recently revised its outlook on natural gas demand, forecasting faster-than-expected growth. According to the IEA, demand is projected to stay elevated into next year, potentially creating supply pressures due to insufficient growth in production. This imbalance between rising demand and slower supply increases could exacerbate challenges in the energy market. As of October 15, European regional storage facilities were 95.02% full, with Denmark and Latvia lagging behind. The European TTF gas benchmark saw moderate growth in Week 42, rising by EUR 1.054/MWh (from EUR 38.919/MWh to EUR 39.973/MWh).

The price of LNG as a bunker fuel in the port of Sines (Portugal) rose by 4 USD this week, reaching 877 USD/MT on October 15. Despite this rise, the price difference between LNG and conventional fuel remained nearly the same: 123 USD in favor of MGO LS, compared to 124 USD a week earlier. On October 15, MGO LS was priced at 754 USD/MT in the port of Sines. For more detailed information, visit the LNG Bunkering section on mabux.com.

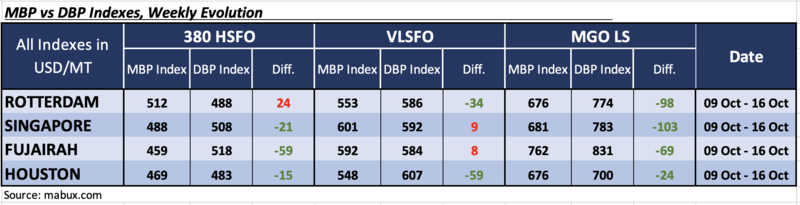

During Week 42, the MDI index (the correlation ratio of market bunker prices (MABUX MBP Index) vs. MABUX digital bunker benchmark (MABUX DBP Index)) revealed the following trends across the four largest global hubs: Rotterdam, Singapore, Fujairah and Houston:

• 380 HSFO segment: Rotterdam remained the only overvalued port, with the weekly average rising by 16 points. The other three ports were undervalued. Weekly averages increased by 16 points in Singapore and 4 points in Houston, but decreased by 1 point in Fujairah.

• VLSFO segment: Singapore and Fujairah remained in the overvalued zone, with weekly averages dropping by 2 points in Singapore and 1 point in Fujairah. Rotterdam and Houston were undervalued, with Rotterdam's weekly average falling by 9 points, while Houston saw a 1-point increase.

• MGO LS segment: All four selected ports were in the undercharge zone. Weekly averages decreased by 20 points in Rotterdam and 9 points in Singapore, but rose by 10 points in Fujairah and 5 points in Houston. The MDI index in Singapore approached the $100 mark, while in Rotterdam it fell below this level.

Overall, the balance of overvalued versus undervalued ports showed little change at the end of the week, with the global trend of undervaluation across all bunker fuel types continuing to dominate.

For more insights into the correlation between market prices and the MABUX digital benchmark, visit the “Digital Bunker Prices” section at mabux.com.

VeriFuel’s latest fuel quality statistics for Q3 2024 highlight volatility in viscosity levels in Very Low Sulfur Fuel Oil (VLSFO), along with some changes in the catalytic abrasive fines (cat fines) content of High Sulfur Fuel Oil (HSFO). The global average viscosity for VLSFO has increased steadily, rising from 115 cSt (at 40 degrees Celsius) in Q1 2021 to 165 cSt in Q3 2024. On a monthly basis, global average viscosity levels have remained relatively stable in 2024, with the exception of notable fluctuations in the ports of Piraeus, Las Palmas, and Santos. The percentage of off-spec VLSFO has also stayed consistent throughout the year. However, Istanbul saw a sharp rise in off-spec VLSFO in the last quarter, with 9.4% of all samples tested being off-spec. For HSFO, quality testing results were generally stable in the third quarter, though there were some shifts in the concentration of cat-fines (Al+Si) in Istanbul, Gibraltar, Algeciras, and Zhoushan. In the ARA region, the average cat fines rates for the first three quarters of 2024 were 49%, 27%, and 61%, respectively. Regarding HSFO off-spec, Cuxhaven (22.2%), Hong Kong (11.1%), and Houston (5.5%) all recorded such cases in Q3, despite no off-spec HSFO being detected in these ports during the first two quarters of the year.

We anticipate that the global bunker market has likely exhausted its downward potential, and next week bunker indices may show a moderate upward correction.

By Sergey Ivanov, Director, MABUX

All news