Significant irregular fluctuations will continue to prevail in the global bunker market in the coming week

The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

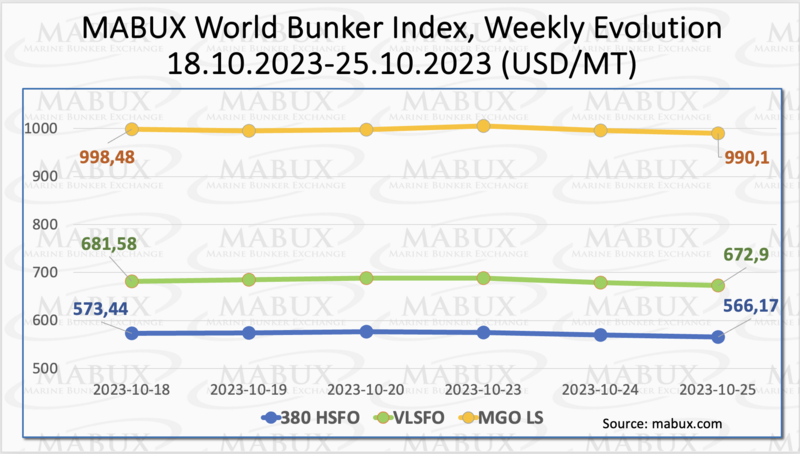

During Week 43, the MABUX global bunker indices resumed again a moderate downward trend. The 380 HSFO index fell by 7.27 USD: from 573.44 USD/MT last week to 566.17 USD/MT. The VLSFO index, in turn, lost 8.68 USD (672.90 USD/MT versus 681.58 USD/MT last week). The MGO index fell by 8.38 USD (from 998.48 USD/MT last week to 990.10 USD/MT, still at the 1000 USD mark. At the time of writing, the market continued to move moderately downward.

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - saw a slight reduction, now standing at minus $1.41 (106.73 USD versus 108.14 USD the prior week), although it remained consistently above the $100.00 mark (SS breakeven). Conversely, the weekly average increased by $1.38. In Rotterdam, SS Spread was up $4.00 (from $82.00 last week to $86.00) and the average rose by $2.34. In Singapore, the difference in the price of 380 HSFO/VLSFO widened by $4.00 ($187.00 versus $183.00 last week), with the weekly average increasing by $2.83. We expect that the SS Spread will maintain moderate growth potential next week. More information is available in the “Differentials” section of www.mabux.com.

The European Union (EU) currently boasts gas storage levels exceeding 97%, while gas consumption remains lower than the levels observed in 2022. Additionally, there is the potential for increased gas exports from the United States. The ongoing conflict in the Middle East is expected to exert a limited upward influence on near-term gas prices, as it reflects a geopolitical risk premium that is already evident in oil prices. Nevertheless, there is a lingering risk of the conflict escalating into a more extensive confrontation, which could temporarily drive up energy prices.

The price of LNG as bunker fuel in the port of Sines (Portugal) has once again decreased, reaching 975 USD/MT on October 23. This marks a drop of 43 USD compared to the previous week. The difference in price between LNG and conventional fuel on October 23 has swung back in favor of LNG, with an 8 USD advantage, as opposed to the 41 USD advantage in favor of MGO just a week earlier. On that day, MGO LS was quoted at 983 USD/MT in the port of Sines. More information is available in the LNG Bunkering section of www.mabux.com.

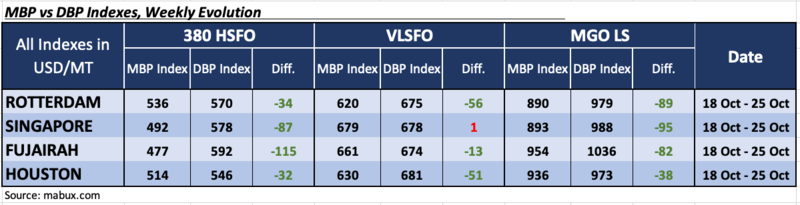

During Week 43, the MDI index (the ratio of market bunker prices (MABUX MBP Index) vs. the MABUX digital bunker benchmark (MABUX DBP Index)) registered the following trends in four selected ports: Rotterdam, Singapore, Fujairah and Houston:

In the 380 HSFO segment, all four ports continued to be undervalued. The average weekly undercharging increased by 5 points in Rotterdam, 5 points in Singapore, 11 points in Fujairah and 5 points in Houston. In Fujairah, the overprice level of this fuel type still exceeded the $100 mark.

For the VLSFO segment, Singapore remained in the overpricing zone according to the MDI, with its weekly average decreasing by 6 points. In the other three ports, VLSFO was underestimated. Undervaluation weekly average increased by 4 points in Rotterdam and 7 points in Fujairah, but decreased by 1 point in Houston. Singapore is nearing a 100% correlation between market prices and the digital benchmark.

In the MGO LS segment, the weekly average level of undervaluation showed a decrease in Rotterdam by 4 points, in Fujairah by 17 points and in Houston by 9 points. In Singapore, the weekly average MDI index remained unchanged.

More information on the correlation between market prices and the MABUX digital benchmark is available in the “Digital Bunker Prices” section of www.mabux.com.

A recent report jointly published by UMAS, the Getting to Zero Coalition, and Race to Zero has concluded that there is still a viable opportunity for scalable zero-emission fuels to constitute 5% of international shipping fuels by 2030, as outlined in the International Maritime Organization's (IMO) Revised GHG Strategy. However, this window of opportunity is rapidly closing, necessitating prompt and decisive action from the industry. On the conservative side, the report highlights that the existing production of zero-emission fuels in the pipeline may cover only a quarter of the fuel demand required to achieve this significant breakthrough. Nevertheless, the report optimistically suggests that, if more projects meet success, zero-emission fuel production could potentially exceed the demand by up to twice the required amount, even when accounting for the fuel needs of other sectors. The report indicates that financing toward the IMO's base target is making some progress, with shipping finance commitments under the Poseidon Principles exceeding $200 billion. Furthermore, the climate alignment of these investments has improved from 4% to 6% on a weighted average basis. However, the report emphasizes that the industry's ability to continue enhancing alignment as regulatory requirements become more stringent remains uncertain and requires careful monitoring.

We expect that amid high volatility triggered by the ongoing conflict in the Middle East, significant irregular fluctuations will continue to prevail in the global bunker market in the coming week.

By Sergey Ivanov, Director, MABUX

All news