The Bunker Outlook was contributed by Marine Bunker Exchange (MABUX)

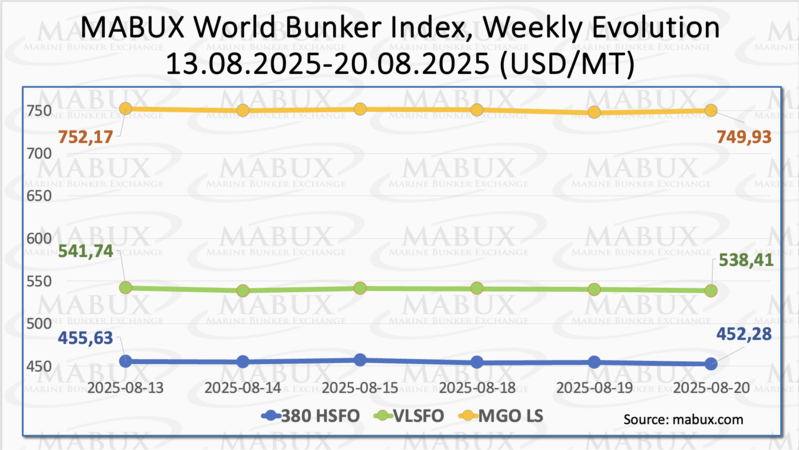

At the close of the 34th week, the global bunker indices MABUX continued their moderate downward trend. The 380 HSFO index fell by 3.35 USD, from 455.63 USD/MT last week to 452.28 USD/MT, moving closer to the 450 USD mark. The VLSFO index declined by 3.33 USD, down to 538.41 USD/MT from 541.74 USD/MT a week earlier. The MGO index also decreased, losing 2.24 USD from 752.17 USD/MT to 749.93 USD/MT, thus breaking below the 750 USD threshold. At the time of writing, the global bunker market showed no clear trend, with indices fluctuating in mixed directions.

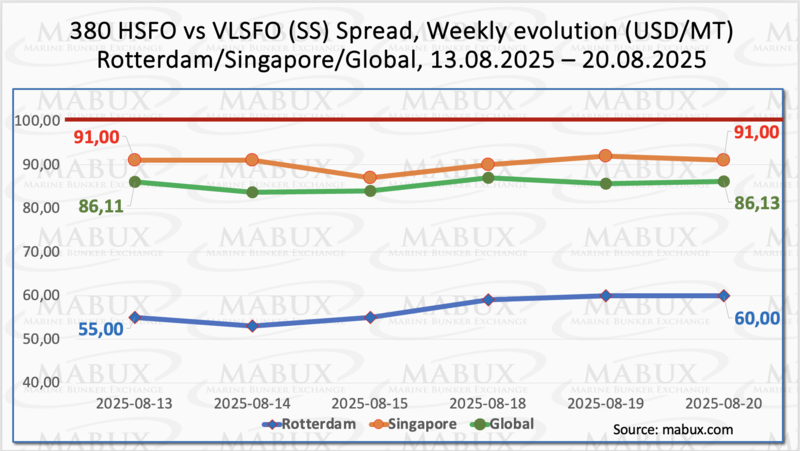

The MABUX Global Scrubber Spread (SS), which represents the price difference between 380 HSFO and VLSFO, remained virtually unchanged over the week, edging up by just $0.02 from $86.11 to $86.13. The indicator continues to stay firmly below the psychological breakeven mark of $100.00. The weekly average of the index also showed a slight increase of $0.62. In Rotterdam, the SS Spread rose by $5.00, reaching $60.00 compared to $55.00 the previous week, with the port’s weekly average gaining $3.17. In contrast, Singapore recorded no change in the 380 HSFO/VLSFO differential, which remained at $91.00, while the port’s weekly average slipped by $1.84. Amid the current stabilization of the global bunker market, significant shifts in the SS Spread are unlikely in the coming week. Conventional VLSFO fuel is expected to retain higher profitability compared with the HSFO plus Scrubber option. Further details can be found in the Differentials section of mabux.com.

U.S. liquefied natural gas (LNG) exports to Europe have risen sharply by 61% year-on-year, driven by the significant depletion of gas storage at the end of the last heating season, which required additional replenishment purchases, lower wind and hydroelectric generation, and the European Union’s commitment to increase imports of U.S. energy as part of its effort to reduce its trade surplus with the United States. In light of these factors, Europe is expected to continue buying as much U.S. LNG as possible, even though prices have already averaged $8.34 per thousand cubic feet in the first eight months of the year.

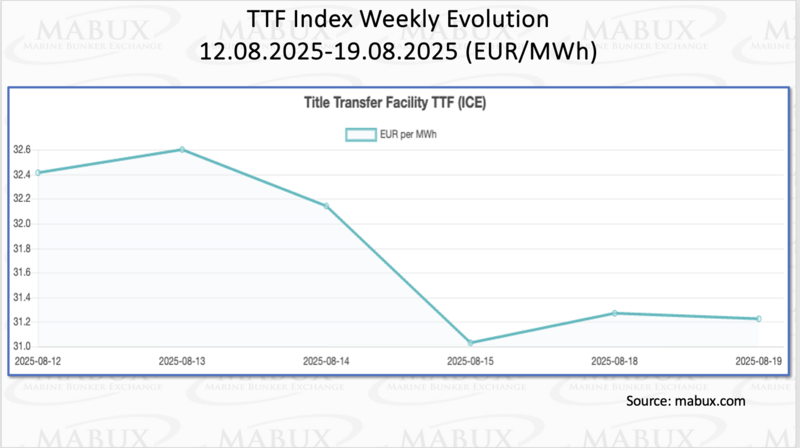

As of 19 August, European regional gas storage facilities were 74.21% full, reflecting an increase of 1.94% compared to the previous week. Occupancy levels are now 2.88% higher than at the beginning of the year, when they stood at 71.33%. However, the pace of injections into storage has slowed slightly. At the close of the 34th week, the European gas benchmark TTF continued its moderate decline, falling by 1.182 euros/MWh to 31.227 euros/MWh, compared with 32.409 euros/MWh a week earlier.

By the end of the week, the price of LNG as a bunker fuel in the port of Sines (Portugal) fell by $27.00, reaching 741 USD/MT compared with 768 USD/MT the previous week. At the same time, the price gap between LNG and conventional fuel narrowed slightly but still favored conventional fuel. On 19 August, the difference stood at 27 USD, down from 39 USD a week earlier, as MGO LS in Sines was quoted at 714 USD/MT. More detailed information is available in the LNG Bunkering section on the mabux.com website.

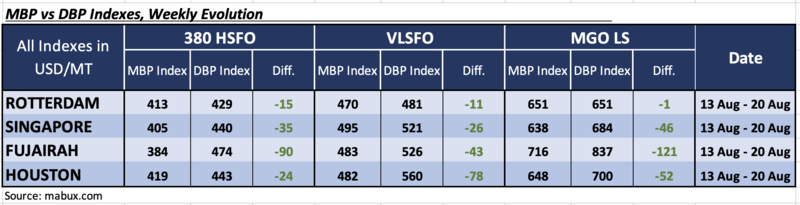

At the end of the 34th week, the MABUX Market Differential Index (MDI)—which reflects the ratio of market bunker prices (MBP) to the digital bunker benchmark MABUX (DBP)—continued to indicate undervaluation across all types of bunker fuel in the world’s largest hubs: Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: The average weekly undervaluation rose by 4 points in Rotterdam, by 5 points in Singapore, and by 8 points in Fujairah, while it declined by 5 points in Houston. Notably, Fujairah’s MDI approached the $100 threshold.

• VLSFO segment: Undervaluation levels remained unchanged in Rotterdam but climbed by 6 points in Singapore, by 9 points in Fujairah, and by 2 points in Houston.

• MGO LS segment: MDI values fell by 3 points in Rotterdam, by 1 point in Singapore, and by 9 points in Fujairah, but edged up by 1 point in Houston. Rotterdam’s MDI remains close to the full 100% MBP/DBP correlation level, while Fujairah continues to trend toward the $100 mark.

Overall, the structure of overvalued and undervalued ports did not undergo significant changes during the week, though there was a noticeable shift toward overvaluation in the MGO LS segment. Based on current dynamics, the emergence of several overvalued ports is likely in the coming week.

More detailed information on the correlation between market bunker prices and the MABUX digital benchmark can be found in the “Digital Bunker Prices” section on the website mabux.com.

In July, sales of marine fuels (including alternatives) in Singapore totaled 4,918,000 metric tons — the highest monthly figure since the start of the year. Sales of very low sulphur fuel oil (VLSFO) stood at 2,372,100 metric tons, down from 2,485,700 metric tons in July 2024 but up from 2,311,000 metric tons in June. High sulphur fuel oil (HSFO) sales reached 1,964,400 metric tons, showing increases both year-on-year and month-on-month. Marine gasoil sales came in at 3,900 metric tons, declining on both annual and monthly comparisons. In contrast, low sulphur marine gasoil sales rose to 416,000 metric tons, marking gains in both year-on-year and month-on-month terms. In the bioblends segment, sales of VLSFO with a biocomponent (80,500 tonnes) were the second-lowest monthly result of the year. HSFO with a biocomponent totaled 35,300 tonnes — up year-on-year but down from June. Bioblend LSMGO was sold for the fourth consecutive month, amounting to 1,800 tonnes. B100 sales hit a record 2,600 tonnes, the highest ever recorded at the world’s largest bunkering hub. After a sharp rise in June to 55,400 tonnes, LNG sales in July fell to 41,500 tonnes — the lowest level since March. No sales of methanol or ammonia were recorded. Over the first seven months of 2025, Singapore sold a total of 31,897,400 tonnes of marine fuel, slightly up from 31,848,200 tonnes in the same period of 2024.

We expect that the global bunker market will continue to stabilize in the coming week, which may in turn support the formation of a moderate upward trend in bunker prices.

By Sergey Ivanov, Director, MABUX