The Bunker Outlook was contributed by Marine Bunker Exchange (MABUX)

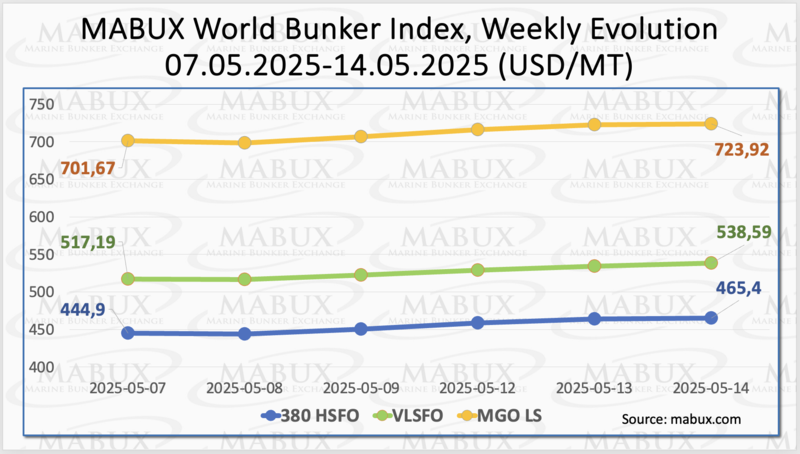

At the end of the 20th week, the global bunker indices MABUX moved upward. The 380 HSFO index rose by $20.50, increasing from $444.90/MT last week to $465.40/MT, once again surpassing the $450.00 mark. The VLSFO index climbed by $21.40, reaching $538.59/MT compared to $517.19/MT the previous week. The MGO index also added $22.25, rising from $701.67/MT to $723.92/MT. At the time of writing, a moderate downward correction was observed in the market.

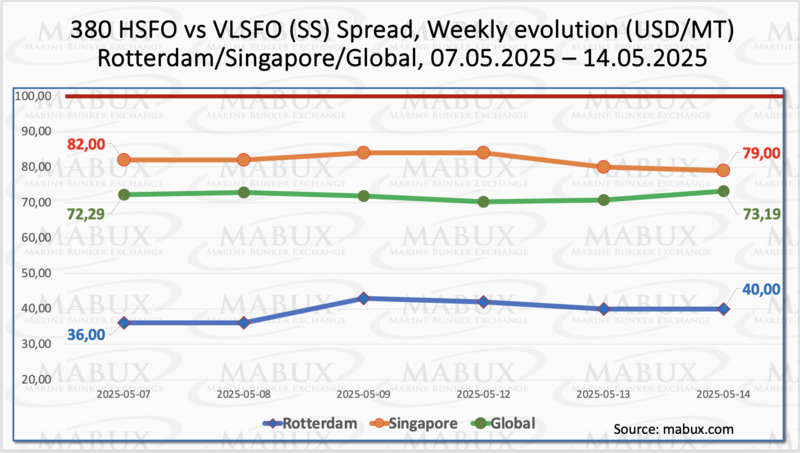

MABUX Global Scrubber Spread (SS) - the difference in price between 380 HSFO and VLSFO - remained virtually unchanged, increasing by $0.90 (from $72.29 last week to $73.19). The average weekly value of the index decreased by a symbolic $0.07. In Rotterdam, SS Spread showed an increase of $4.00 ($40.00 against $36.00 last week). At the same time, the average weekly value in the port also increased by $5.17. In Singapore, the difference in price 380 HSFO/VLSFO, on the contrary, decreased by $3.00, from $82.00 last week to $79.00, and the average weekly value in the port added $12.66. At the moment, there is no pronounced trend in the dynamics of the global and port SS Spread indices and values continue to fluctuate significantly below the $100.00 mark (SS Breakeven). We believe that there will be no significant changes in the dynamics of SS Spread next week. More information is available in the "Differentials" section of www.mabux.com.

Gas prices in Europe have declined by approximately 20% since the end of the heating season. The European Parliament has endorsed the European Commission’s proposal to extend the EU gas storage target through 2027. Under the revised framework, the mandatory storage target has been lowered from 90% to 83%, to be achieved between 1 October and 1 December. In cases of market instability, a deviation of up to 4% may be permitted. Nevertheless, total storage capacity across Member States must not fall below 75%, even with the adopted exceptions and provisions.

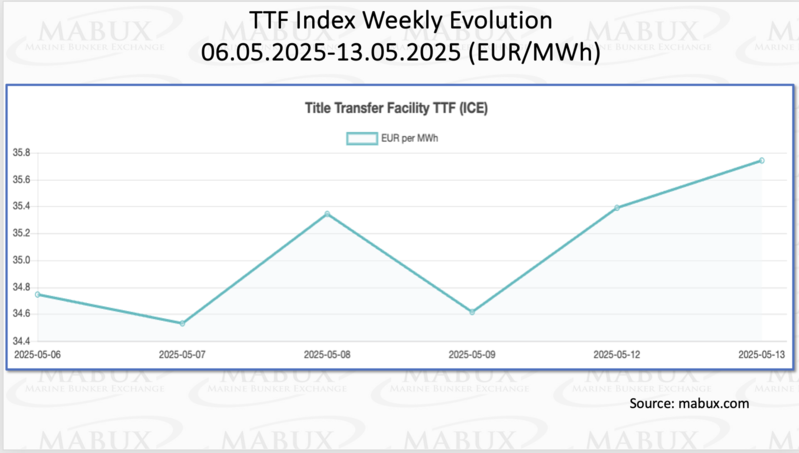

As of May 13, European regional storage facilities were filled to 43.13% (plus 1.72% compared to the previous week and minus 28.20% compared to the beginning of the year (71.33%)). The trend towards gradual filling of gas storage facilities continues. At the end of the 20th week, the European gas benchmark TTF continued its moderate growth: plus 1.001 euro/MWh (35.744 euro/MWh against 34.743 euro/MWh last week).

The price of LNG as a bunker fuel at the Port of Sines (Portugal) decreased by $14 over the week, reaching $720/MT compared to $734/MT the previous week. At the same time, the price gap between LNG and conventional fuel narrowed to $47 in favor of conventional fuel, down from $77 the week before. On May 12, MGO LS was quoted at $673/MT in the Port of Sines. More detailed information is available in the LNG Bunkering section on the mabux.com website.

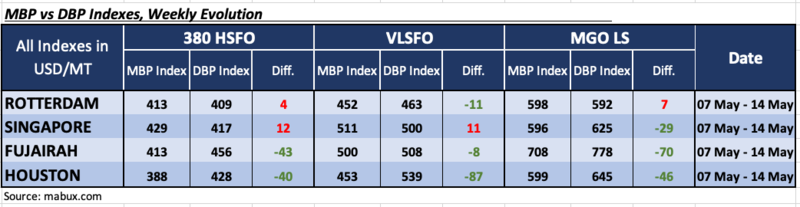

At the end of the 20th week, the MABUX Market Differential Index (MDI) – which reflects the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP) – showed the following trends across the 380 HSFO, VLSFO, and MGO LS segments:

• 380 HSFO segment: Rotterdam and Singapore remained in overvaluation territory, with weekly MDI averages rising by 2 and 1 points, respectively. The other two ports were undervalued: Fujairah saw a 4-point decrease in its undervaluation level, while Houston's undervaluation increased by 6 points. Notably, Rotterdam maintained 100% correlation between MBP and DBP.

• VLSFO segment: Singapore shifted into overvaluation territory this week, with its average weekly MDI rising by 12 points. Rotterdam, Fujairah, and Houston remained undervalued. The MDI decreased by 8 points in both Rotterdam and Fujairah but increased by 5 points in Houston. Fujairah approached 100% correlation between MBP and DBP.

• MGO LS segment: Rotterdam continued as the only overvalued port in this segment, with its weekly MDI rising by 1 point. The other three ports remained undervalued: MDI rose by 7 points in Singapore and 17 points in Houston, while it fell by 6 points in Fujairah. Rotterdam remained close to a 100% correlation between MBP and DBP.

There were no major shifts in the overall overvaluation/undervaluation balance during the week, aside from Singapore’s move into the overvalued zone in the VLSFO segment. No significant adjustments are expected in the valuation dynamics next week.

For further details on the correlation between market prices and the MABUX digital benchmark, please visit the Digital Bunker Prices section at www.mabux.com.

According to DNV’s latest report, 49 new alternative-fuel ship orders were recorded in April, including two hydrogen-powered cruise ships—the first such order since June 2024. Despite a decline in overall newbuilding activity, alternative-fuel orders rose 5% year-on-year. Of these, 24 were methanol-powered and 20 LNG-powered. Methanol orders were mainly in the containership (14) and RoPax (9) sectors, with one tanker contract. LNG orders were distributed across containerships (16), cruise (2), and RoPax (2). DNV highlights increased diversification in alternative fuel adoption, with growth in the RoPax, cruise, and other segments. The rise in methanol and LNG orders reflects a shift in sustainable fuel strategies, with methanol rebounding after a slow start to the year and LNG gaining traction, particularly in the container sector. DNV notes that shipowners are prioritizing flexibility, fuel availability, and segment-specific needs in their decision-making.

We anticipate the global bunker market will likely maintain its potential for a continued moderate upward trend next week.

By Sergey Ivanov, Director, MABUX