The instability in Global bunker market continues and bunker indices may have sharp irregular fluctuations next week

The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

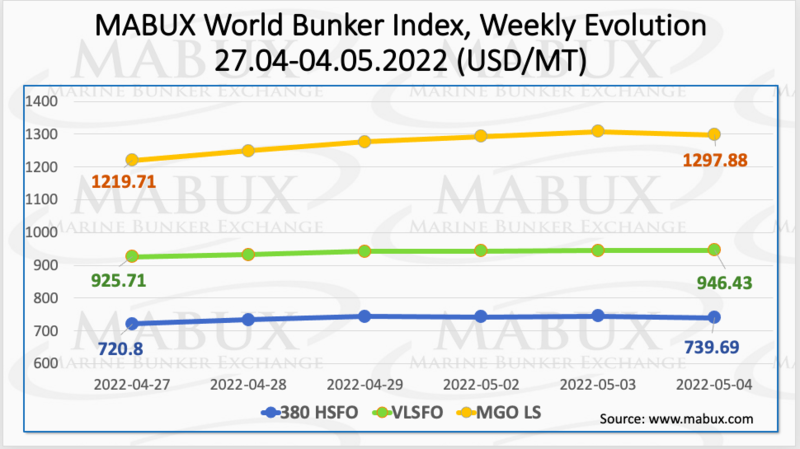

Over the Week 18, global bunker indices turned again into an uptrend. The 380 HSFO index rose by 18.89 USD: from 720.80 USD/MT to 739.69 USD/MT. The VLSFO index went up by 20.72 USD: from 925.71 USD/MT to 946.43 USD/MT. The MGO index rose most significantly: by 78.17 USD (from 1219.71 USD/MT to 1297.88 USD/MT). The ongoing military conflict in Ukraine keeps the global bunker market highly volatile.

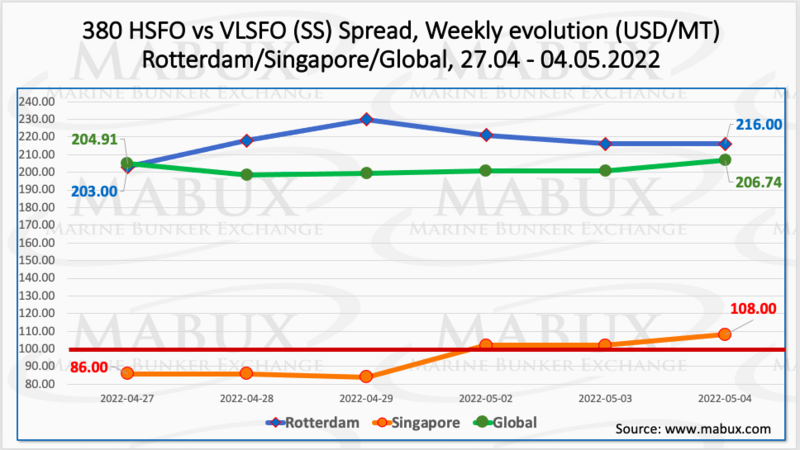

The Global Scrubber Spread (SS) weekly average - the price difference between 380 HSFO and VLSFO - continued its moderate decline over the week - minus $8.09 ($201.83 versus $209.92 last week). At the same time, the difference in absolute values increased by $1.83 at the end of the week. In Rotterdam, the average SS Spread also dropped from $224.83 to $217.33 (down $7.50 from last week), but the difference in the SS Spread’s absolute values rose by $13.00 at the end of the week. The 380 HSFO/VLSFO price difference at the port of Singapore continued to narrow over Week 18, with the average dropping another $9.66 and falling below the $100 psychological mark ($94.67 vs. $104.33 last week). We believe that the reduction in SS Spread in Singapore is temporary as it remains consistently above $100 in other regions. For more information, see the Price Differences section of mabux.com.

The increase in LNG prices seems to be continuing to have an impact on LNG bunker volumes Europe and in Rotterdam, in particular. The 111,804 cubic metres (cbm) sold at the port in the latest quarter was up on the 94,454 cbm sold in Q4 2021, but was still down significantly on the 212,719 cbm total for Q3 2021 (which is still Rotterdam’s highest quarterly LNG bunkering volume to date).

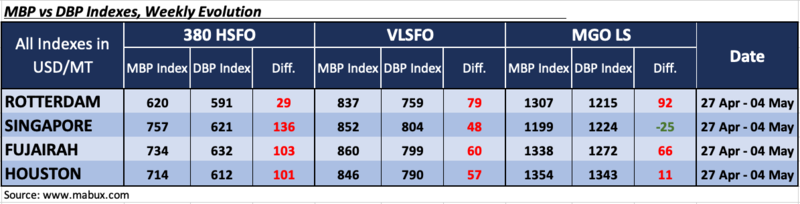

Over the Week 18, the average correlation of MABUX MBP Index (market bunker prices) vs MABUX DBP Index (MABUX digital bunker benchmark) was mostly in the overcharge zone. Thus, 380 HSFO fuel was overpriced by $29 in Rotterdam, by $125 in Singapore, by $103 in Fujairah and by $101 in Houston. The MABUX MBP/DBP Index (MBI) in the 380 HSFO segment did not have any firm trend over the week: the overcharge premium decreased in Rotterdam and Houston, while it increased in Singapore and Fujairah.

VLSFO fuel grade, according to the MBI index, was also overpriced in all selected ports: plus $79 in Rotterdam, plus $48 in Singapore, plus $60 in Fujairah and plus $57 in Houston. Here, the changes in the MBI index also did not have a single trend: the overcharge premium increased in Fujairah, decreased in Rotterdam and Houston, but did not change in Singapore.

As for MGO LS, for the first time in the last two months, the MBI index registered an average underestimation of this fuel grade: Singapore - minus $ 25. In other selected ports, MGO LS fuel remained overvalued: Rotterdam - plus $ 92, Fujairah - plus $ 66 and Houston - plus $ 11. In general, in the MGO LS segment, there has been a reduction trend in fuel overcharge premium in all ports.

The volumes of high sulphur fuel oil (HSFO) and ultra low sulphur fuel oil (ULSFO) sold in the Port of Rotterdam in the first quarter of 2022 were up y-o-y by around 14% and 41% respectively at 706,491 tonnes and 284,134 tonnes – but very low sulphur fuel oil (VLSFO) sales were down around 1% at 966,223 tonnes. Although HSFO sales were up on the first quarter of 2022, they were down on the preceding quarter – Q4 2021 – when the port’s suppliers delivered 745,271 tonnes of the high sulphur product. Given that the Russia-Ukraine conflict has already had an impact on Rotterdam’s fuel oil cargo volumes – there may well be a further drop in HSFO bunker sales in the Q2 figures.

As per new Q1 2022 statistics from Bureau Veritas VeriFuel, some 4.3% of very low sulphur fuel oil (VLSFO) fuel samples in the ARA region were off-spec in Q1 2022. Sulphur content was the ‘culprit’ in the ARA, while sediment was the reason for 3.3% of off-spec samples in Malta, followed by 2.9% in Istanbul, caused by density issues. From a global ports perspective, there were minimal changes quarter on quarter in terms of meeting ISO 8217 specifications. The global average of off-spec fuel samples due to sulphur content was 1.7%, up on the 1.3% seen in the last quarter of 2021 but down in comparison to the first quarter of last year, where it was 2.2%.

The instability in Global bunker market continues. We expect bunker indices may have sharp irregular fluctuations next week.

By Sergey Ivanov, Director, MABUX

All news