The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

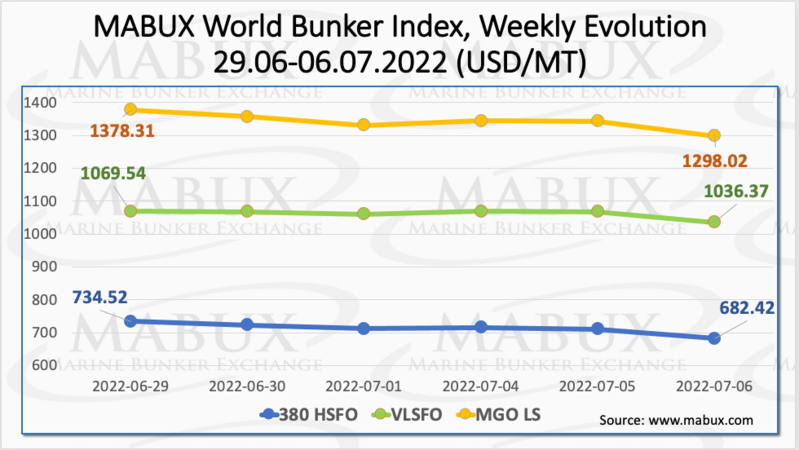

Over the Week 27, the world bunker indices showed a sharp decline, primarily due to the fall in oil prices on July 05. The 380 HSFO index fell by 52.10 USD: from 734.52 USD/MT to 682.42 USD/MT. The VLSFO index, in turn, decreased by 33.17 USD: from 1069.54 USD/MT to 1036.37 USD/MT. The MGO Index suffered the most significant losses: minus 80.29 USD (from 1378.31 USD/MT to 1298.02 USD/MT), dropping below 1300 USD.

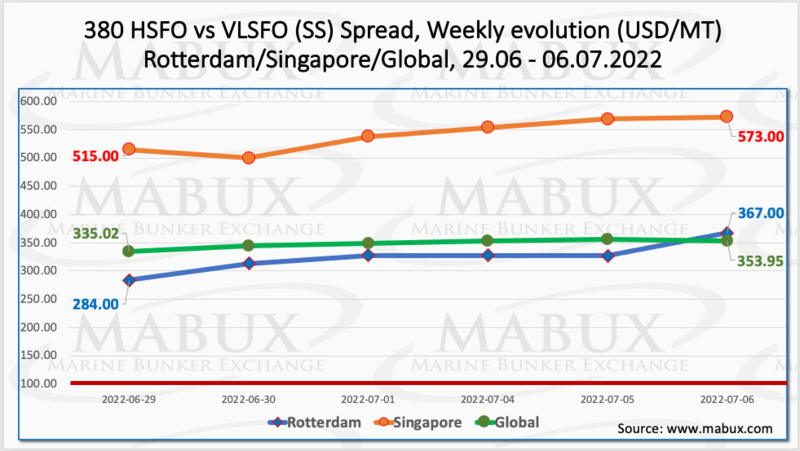

Despite the decline in fuel prices, the Global Scrubber Spread (SS) weekly average - the price difference between 380 HSFO and VLSFO - continued to increase over the week - plus $ 14.70 ($ 348.90 vs. $ 334.20 last week). In Rotterdam, the average SS Spread also rose: $324.50 vs. $307.00 (up $17.50 from last week). The most significant growth in the average weekly 380 HSFO/VLSFO price difference was registered in Singapore: plus $ 51.67, breaking the $ 500 mark: $ 541.50 versus $ 489.83 last week. For more information, please visit the Price Difference section on mabux.com.

Tight supply and energy security uncertainty pushed natural gas prices to record highs over the week. The price of LNG as bunker fuel in the port of Sines (Portugal) rose on July 4 by 193 USD, exceeding 3000 USD mark: 3156 USD/MT (versus 2963 USD/MT a week earlier). LNG prices are more than double those of traditional bunker fuels: MGO LS at the port of Sines was quoted on July 06 at 1426 USD/MT.

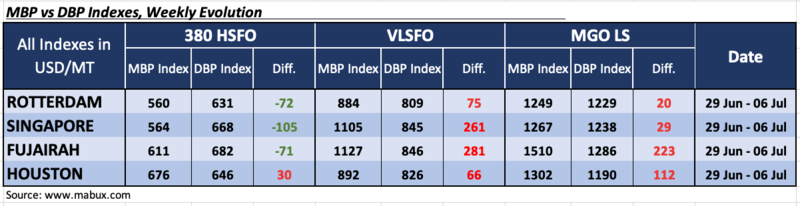

Over the Week 27, the MDI index (comparison of MABUX MBP Index (market bunker prices) vs MABUX DBP Index (MABUX digital bunker benchmark)) continued to register an underestimation of 380 HSFO fuel in three out of four ports selected: Rotterdam - minus $ 72, Singapore - minus $ 105 and Fujairah - minus $71. Houston remains the only overpriced port - plus $ 20. The underprice premium rose in all three ports. In Houston, the overcharge margin continued to decline, approaching 100-percent correlation’s mark.

VLSFO fuel grade, according to MDI, remained overpriced in all four selected ports: plus $75 in Rotterdam, plus $261 in Singapore, plus $281 in Fujairah and plus $66 in Houston. Here, the MDI index did not have a firm trend: the overprice premium increased in Rotterdam, Singapore and Fujairah, but decreased in Houston. VLSFO fuel remains the most overvalued segment in the global bunker market.

As for MGO LS grade, MDI registered an overcharge of this fuel in all selected ports: in Rotterdam - plus $ 20, in Singapore - plus $ 29, in Fujairah - plus $ 223 and in Houston - plus $ 112. The most significant changes were in Fujairah - plus 76 points and Houston - plus 63 points. In Rotterdam and Singapore, over the week, overcharge premium decreased, while in Fujairah and Houston it rose.

DNV reported there were just six vessels added to DNV’s database in June but in spite of a quiet month for contracting, Q2 2022 was the strongest ever quarter for LNG-fuelled tonnage orders, with 83 vessels added to the tally. Meantime, while six orders were placed last month, an adjustment to a previously reported containership booking meant that net growth in June was actually only two additional vessels. Looking ahead to the next few months, however, the LNG bunkering market looks set to witness a ‘ketchup-bottle effect’, with LOIs in the pipeline and reports of ‘numerous’ container vessel and car carrier orders. DNV also highlighted growing momentum in methanol-fuelled vessel orders, with two offshore construction vessels added to its database in June.

We expect next week the global bunker market to pass into upward correction after a sharp fall this week.

By Sergey Ivanov, Director, MABUX

All news