The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

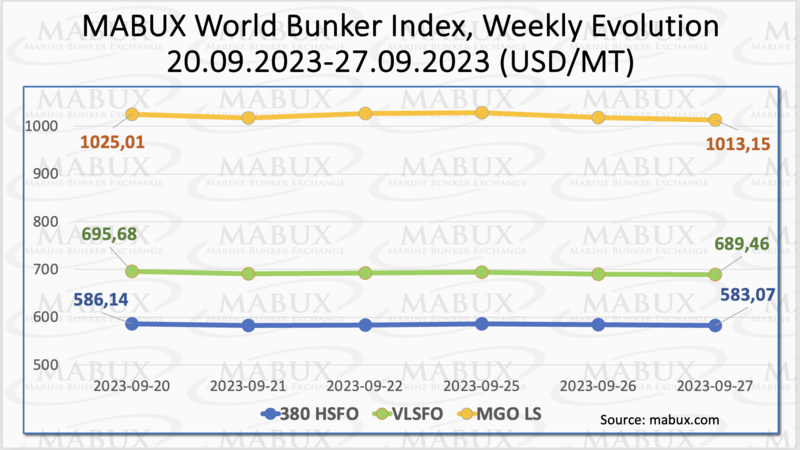

Over the Week 39, the MABUX global bunker indices turned into a moderate decline for the first time in the last four weeks. The 380 HSFO index fell by 3.07 USD: from 586.14 USD/MT last week to 583.07 USD/MT. The VLSFO index, in turn, lost 6.22 USD (689.46 USD/MT versus 695.68 USD/MT last week). The MGO index fell by 11.86 USD (from 1025.01 USD/MT last week to 1013.15 USD/MT), still above the 1000 USD mark. At the time of writing, bunker indices have resumed an upward trend.

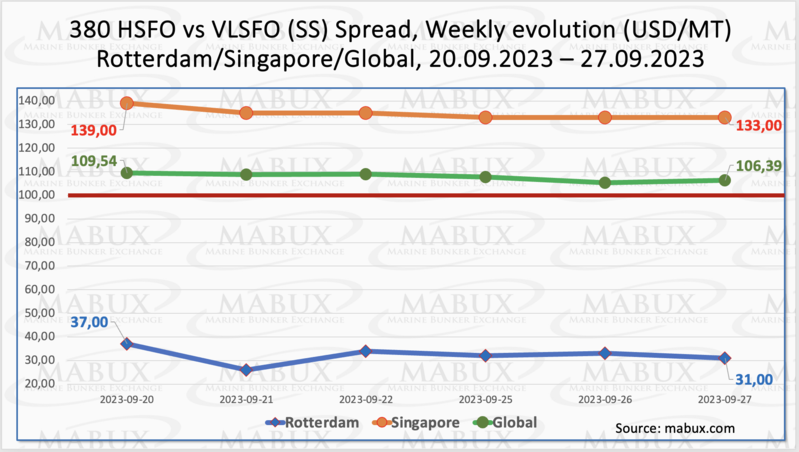

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - again showed a decrease of $3.15 ($106.39 vs. $109.54 last week), still hovering at the $100.00 mark (SS breakeven). Meanwhile, the weekly average increased slightly by $1.19. In Rotterdam, SS Spread dropped by $6.00 from $37.00 last week to $31.00. The average weekly SS Spread in Rotterdam, on the contrary, increased by $3.34. In Singapore, the price difference between 380 HSFO and VLSFO decreased by $6.00 ($133.00 versus $139.00 last week), while the weekly average rose by $15.50. We do not expect a sustainable trend in the SS Spread dynamics for the following week. More information is available in the “Differentials” section of www.mabux.com.

Benchmark natural gas prices in Europe and the UK experienced an early drop following the resolution of a labor dispute between Chevron and trade unions, resulting in the cancellation of strikes at two significant LNG export facilities in Australia. European prices have been marked by substantial volatility in recent weeks, primarily attributed to the strikes in Australia and operational issues at major U.S. LNG export facilities. Additionally, European gas prices witnessed a decline as the substantial Troll gas field in Norway resumed production and began increasing its exports to Europe after an extended maintenance period.

Nevertheless, the price of LNG as bunker fuel in the port of Sines (Portugal) surged, reaching 994 USD/MT on September 25 (plus 154 USD compared to the previous week). The difference in price between LNG and conventional fuel on September 25 decreased significantly: 58 USD in favor of LNG versus 214 USD a week earlier: MGO LS was quoted that day in the port of Sines at 1052 USD/MT. More information is available in the LNG Bunkering section of www.mabux.com.

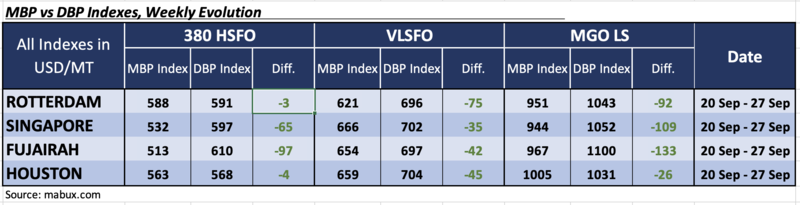

During Week 39, the MDI index (the ratio of market bunker prices (MABUX MBP Index) to the digital bunker benchmark MABUX (MABUX DBP Index)) recorded underpricing of all types of bunker fuels in the selected ports.

Thus, in the 380 HSFO segment, the average weekly underpricing increased in all ports: by 13 points in Rotterdam, by 33 points in Singapore, by 19 points in Fujairah and by 3 points in Houston.

For the VLSFO segment, according to the MDI, the average undervaluation index increased by 11 points in Rotterdam, 9 points in Singapore, 5 points in Fujairah and 12 points in Houston.

In the MGO LS segment, the average underpricing premium increased in Rotterdam by 3 points and in Singapore by 13 points, but decreased in Fujairah by 3 points and in Houston by 12 points.

Hence, the trend of undervaluation in the global bunker market continues. More information on the correlation between market prices and the MABUX digital benchmark is available in the “Digital Bunker Prices” section of www.mabux.com.

The International Energy Agency (IEA) said the world would not need any new long lead-time conventional oil and gas projects or coal mines approved after 2023 as the surge in clean energy deployment could lead to peak fossil fuel demand this decade. The new report, an update on the first such publication from 2021, takes into account the developments in the energy sector in the past two years, including the energy crisis, the conflict in Ukraine, the drive for energy security, and the surge in solar installations and electric vehicle sales. It is predicted, that in a net-zero (NZE) scenario, demand for oil and gas is set to decline by around 20% by 2030. However, the agency noted that investment in existing fossil fuel supply projects is still needed in the NZE Scenario “to ensure that supply does not fall faster than the decline in demand.” The IEA also warned that an “orderly” energy transition is far from certain, especially if fossil fuel investment falls faster than clean energy expansion catching up, or if low-cost resource holders decide to tap more oil and gas to boost their market share and influence fossil fuel prices by restricting production.

We expect that next week there will be no a sustainable trend in the global bunker market, while bunker prices will change irregular.

By Sergey Ivanov, Director, MABUX

All news