Moderate downward trend in the global bunker market is expected to continue next week

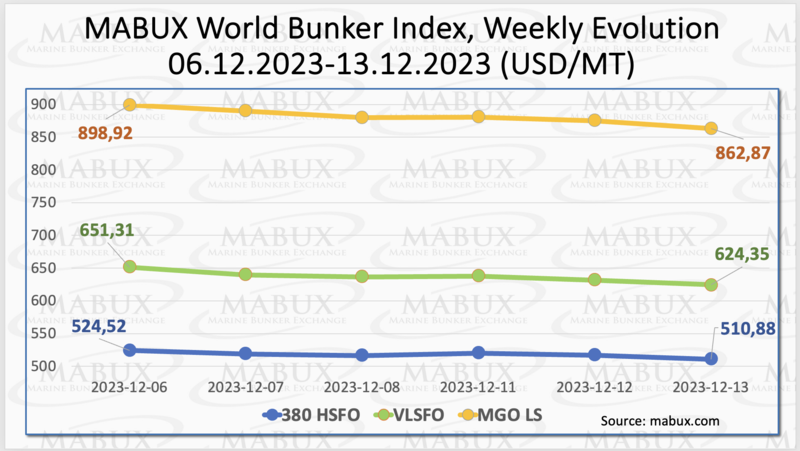

As of Week 50, the MABUX global bunker indices continued steady downward trend. Index 380 HSFO dropped by 13.64 USD: from 524.52 USD/MT last week to 510.88 USD/MT, nearing the 500 USD mark. Index VLSFO lost 26.96 USD (624.35 USD/MT versus 651.31 USD/MT the previous week). Index MGO fell by 36.05 USD (from 898.92 USD/MT last week to 862.87 USD/MT). At the time of writing global bunker indices continued to trend downwards.

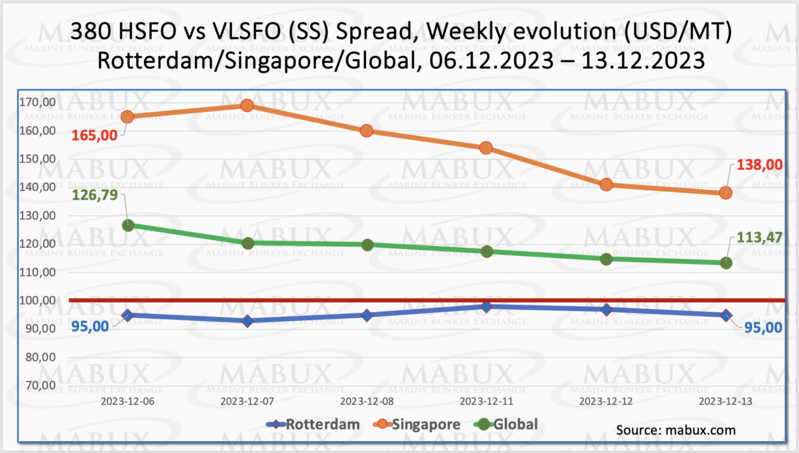

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - showed a further reduction: minus $13.32 ($113.47 versus $126.79 last week), gradually approaching the $100.00 mark (SS breakeven). At the same time, the weekly average decreased by $14.38. In Rotterdam, SS Spread remained unchanged at the end of the week, staying at $95.00, while the weekly average increased by $3.17. The most significant decline in the 380 HSFO/VLSFO price difference was once again recorded in Singapore: minus $27 ($138.00 versus $165.00 last week), with the weekly average also decreasing by $13.67. We expect the downward trend to persist in SS Spread next week. More information is available in the "Differentials" section of www.mabux.com.

European gas storages are currently operating at 94% capacity, with weather forecasts predicting favorable wind generation and above-normal temperatures throughout Europe. Despite an increase in heating demand, European natural gas prices have continued to decrease. This trend can be attributed to the anticipated mild December temperatures, consistently high storage levels, robust Norwegian gas flow, and active LNG send-out. The market foresees that ample supply and substantial storage capacity will counteract any upward price pressures, even as gas demand is expected to rise during the winter season.

The price of LNG as bunker fuel in the port of Sines (Portugal) continued to decline and reached 808 USD/MT on December 12 (minus 84 USD compared to last week). Meantime, the difference in price between LNG and conventional fuel as of December 12 was 22 USD in favor of LNG versus 18 USD in favor of MGO a week earlier: MGO LS was quoted on this day at the port of Sines at 830 USD/MT. More information is available in the LNG Bunkering section of www.mabux.com.

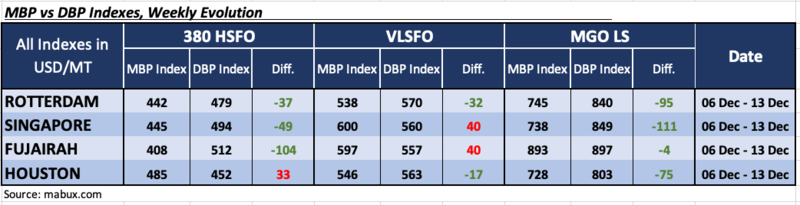

During the 50th week, the MDI index (the ratio of market bunker prices (MABUX MBP Index) vs. the MABUX digital bunker benchmark (MABUX DBP Index)) recorded the following trends in four selected ports: Rotterdam, Singapore, Fujairah and Houston:

In the 380 HSFO segment, Houston was the only overpriced port, with the overprice weekly average increasing by 27 points. The other three ports remained in the undercharge zone. Weekly average increased by 7 points in Rotterdam and decreased by 1 point in Singapore. The MDI index in Fujairah remained unchanged, still exceeding the $100 mark.

In the VLSFO segment, according to the MDI, Singapore and Fujairah were in the overcharge zone, with the average weekly premium increasing by 1 point in Singapore and 8 points in Fujairah. In Rotterdam and Houston, VLSFO remained undervalued. Weekly average levels of undercharging fell by 3 points in Rotterdam and 6 points in Houston.

In the MGO LS segment, all ports remained undervalued. The weekly average widened in Rotterdam by 2 points and in Houston by 4 points, but narrowed in Singapore by 4 points and in Fujairah by 15 points. Singapore remains the only port where the level of underpricing exceeds $100 mark.

All in all, there is still no stable trend in the dynamics of the MDI index in the world's largest hubs during the week.

More information on the correlation between market prices and the MABUX digital benchmark is available in the “Digital Bunker Prices” section of www.mabux.com.

The latest report from the United States Central Intelligence Agency (CIA) on global commercial fleets positions Iran at 25th place, surpassing countries like the United States, Germany, and France. According to the report, Iran boasts a fleet of 924 commercial vessels, securing its position among 186 nations. Notably, countries such as Brazil, Portugal, Denmark, Canada, Germany, Australia, Bangladesh, Spain, and Switzerland have smaller fleets compared to Iran. This assessment aligns with the findings of the United Nations Conference on Trade and Development (UNCTAD) in January, which ranked Iran as the owner of the world's 22nd-largest maritime fleet in terms of capacity. UNCTAD's data revealed that the global count of commercial ships, encompassing tankers, container ships, and bulk carriers, reached 55,037 by the end of 2022. The cumulative capacity of these vessels amounted to 2,180,058,307 tons in 2022, reflecting a two percent increase from the preceding year.

We expect the moderate downward trend in the global bunker market to continue next week.

By Sergey Ivanov, Director, MABUX

All news