The Bunker Outlook was contributed by Marine Bunker Exchange (MABUX)

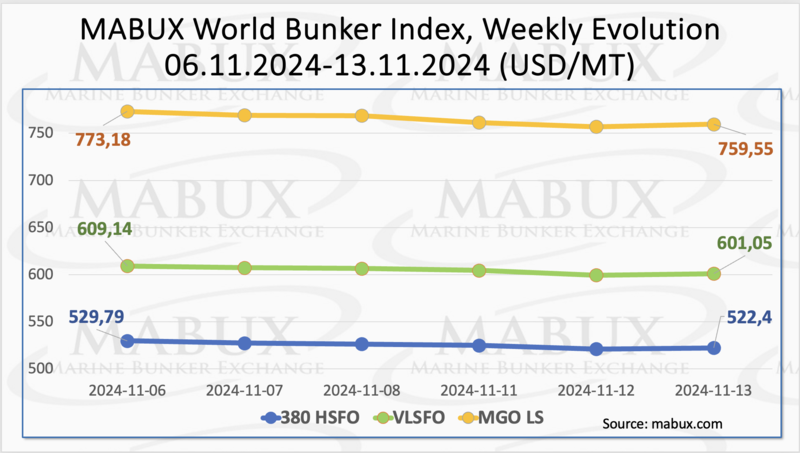

In Week 46, the MABUX global bunker indices shifted back to a moderate downward trend. The 380 HSFO index fell by 7.39 USD: from 529.79 USD/MT last week to 522.40 USD/MT. The VLSFO index decreased by 8.09 USD (601.05 USD/MT versus 609.14 USD/MT last week), approaching the 600 USD mark. The MGO index declined by 13.63 USD (from 773.18 USD/MT last week to 759.55 USD/MT). At the time of writing, a slight upward correction was observed in the global bunker market.

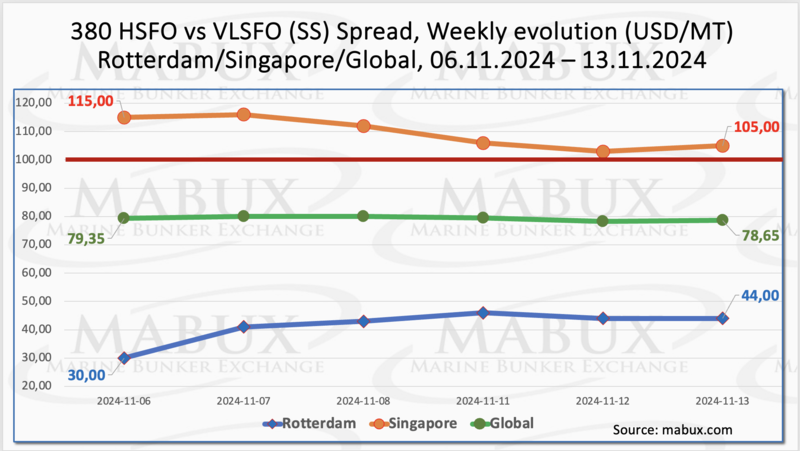

MABUX Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - saw a slight reduction of $0.70 (from $79.35 last week to $78.65), remaining below the $100.00 SS Breakeven threshold. In contrast, the weekly average increased by $7.57. In Rotterdam, the SS Spread grew by $14.00 (from $30.00 to $44.00), with the weekly average up by $21.00. In Singapore, the 380 HSFO/VLSFO price difference fell by $10.00: from $115.00 last week to $105.00, approaching again the $100.00 mark, although the weekly average rose by $2.00. Overall, the SS Spread showed no consistent trend during the week, with values remaining near or below the $100.00 mark. No sustainable trend is expected next week for the 380 HSFO and VLSFO price differential. More information is available in the Differentials section of www.mabux.com.

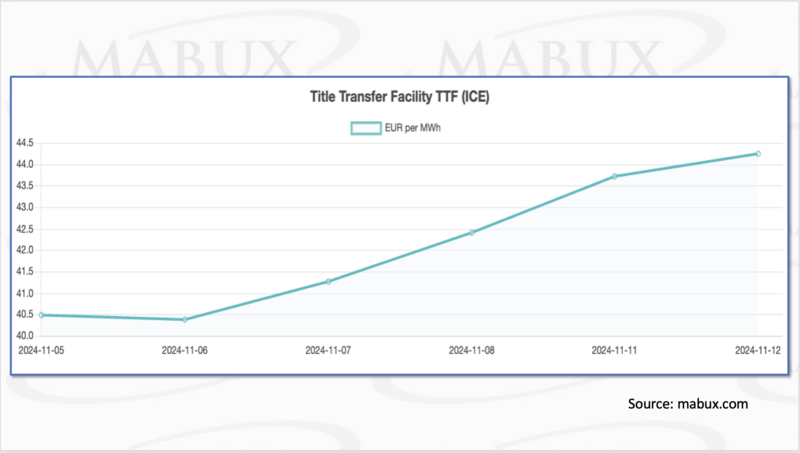

European gas prices have recently surged due to concerns over supply stability, driven by escalating tensions in the Middle East and unplanned outages in Norway, Europe’s largest gas supplier. Further adding to these concerns is the upcoming expiration of the Ukraine-Russia agreement on Russian gas transit to Europe via Ukraine, set for December 31, 2024. However, the rise in European gas prices has attracted additional LNG shipments. According to data from Kpler, LNG imports into Europe climbed to 7.54 million metric tons in October, up from 6.37 million tons in September and marking the highest monthly import volumes since May. As of November 11, European regional storage facilities were 93.04%, down 2.29% from the previous week. By the close of Week 46, the European gas benchmark TTF had risen by 3.763 euros/MWh, reaching 44.255 euros/MWh (compared to 40.492 euros/MWh the previous week).

The price of LNG as bunker fuel at the port of Sines, Portugal, increased by USD 79 this week compared to the previous week, reaching USD 927/MT on November 11. Meanwhile, the price difference between LNG and conventional fuel also widened significantly: the spread in favor of MGO LS rose to USD 195 from USD 105 a week earlier. On this date, MGO LS was quoted at USD 732/MT at the port of Sines. More details can be found in the LNG Bunkering section on www.mabux.com.

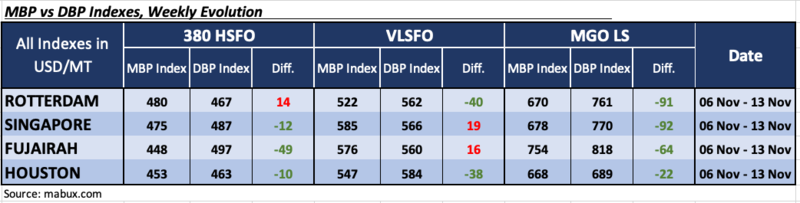

During Week 45, the MDI index (the correlation ratio of market bunker prices (MABUX MBP Index) vs. MABUX digital bunker benchmark (MABUX DBP Index)) registered the following trends across the four largest global hubs: Rotterdam, Singapore, Fujairah and Houston:

• 380 HSFO segment: Singapore and Houston returned to the underchange zone, joining Fujairah. Weekly averages increased by 13 points in Singapore, 6 points in Fujairah, and 18 points in Houston. Rotterdam remained the only overvcharged port in this bunker segment, with a weekly average decrease of 26 points.

• VLSFO segment: Singapore and Fujairah remained in the overcharge zone, with weekly averages dropping by 12 points in Singapore and 3 points in Fujairah. Rotterdam and Houston were undervalued. Weekly averages rose by 5 points in Rotterdam but fell by 8 points in Houston.

• MGO LS segment: All four selected ports remained undervalued. Weekly averages increased by 3 points in Rotterdam, 6 points in Singapore, and 9 points in Fujairah, with Houston’s average decreasing by 1 point. MDI readings across all ports remained below the $100.00 mark.

At the end of the week, the balance of overvalued/undervalued ports shifted toward underpricing of fuel. We expect the undercharge trend to continue into next week.

According to DNV, October saw a record month for methanol-powered vessel orders in 2024, with 29 total orders, 20 of which came from the bulk carrier segment. Despite methanol’s strong showing, LNG remained the leader in alternative-fuel vessel orders. Of the 66 orders placed in October, 58 were for vessels in the container segment. In the first 10 months of 2024, 464 new alternative-fuel vessel orders have been recorded, marking a 46% year-on-year increase, with LNG orders in the lead. Since July, 177 new LNG vessel orders have been placed, up from 52 in the first half of the year, driven largely by a surge in container activity. Methanol is also gaining traction, with 162 methanol-powered vessel orders in 2024 so far, already exceeding the total for 2023.

Bunker fuel prices in the market lack clear directional dynamics and are moving sideways. This trend is expected to persist into the following week.

By Sergey Ivanov, Director, MABUX

All news