The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

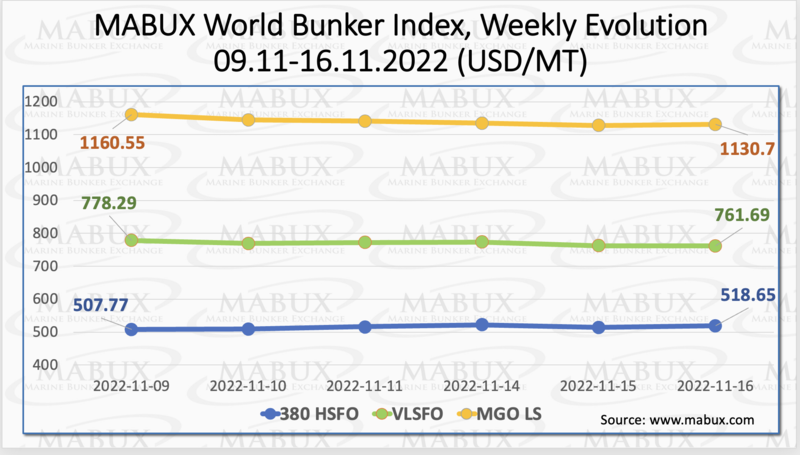

Over the Week 46, MABUX global bunker indices demonstrated irregular changes. The 380 HSFO index rose by 10.88 USD: from 507.77 USD/MT last week to 518.65 USD/MT, being still above the 500 USD mark. The VLSFO index, in turn, fell by 16.60 USD (761.69 USD/MT versus 778.29 USD/MT last week). The MGO index also lost 29.85 USD (from 1160.55 USD/MT to 1130.70 USD/MT), continuing its decline towards 1100 USD mark. Index’s irregular fluctuations showed the absence of a sustainable trend in the global bunker market.

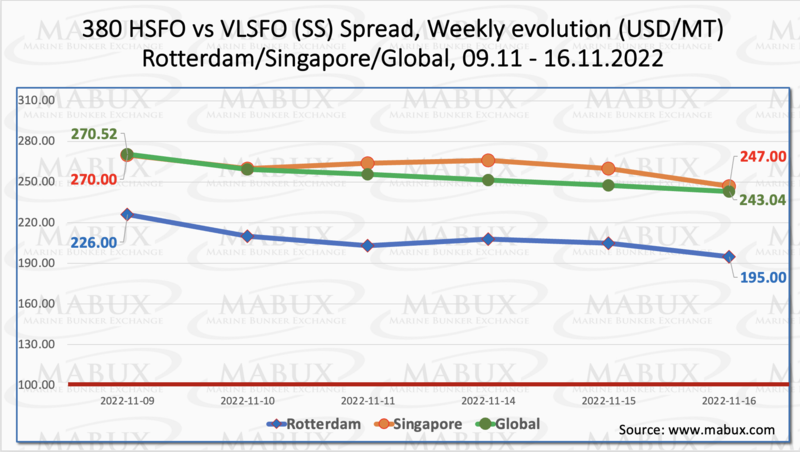

Global Scrubber Spread (SS) - the price differential between 380 HSFO and VLSFO - continued its firm decline over the week 46 - minus $ 27.48 ($ 243.04 vs. $ 270.52 last week), breaking through $ 250 level. In Rotterdam, SS Spread also decreased by $31.00 to $195.00 from $226.00 last week, falling below the $200 mark for the first time since October 04 this year. In Singapore, the 380 HSFO/VLSFO price difference has dropped by $23.00 ($247.00 from $270.00 last week). We expect SS Spread to continue narrowing next week. More information is available in the Differentials section at mabux.com.

The benchmark natural gas prices in Europe and the United States jumped as forecasts point to below-normal temperatures across most of America and a cold spell in northwest Europe this week. The price of LNG as bunker fuel at the port of Sines (Portugal) rose to 1716 USD/MT on November 14 (plus 181 USD compared to the previous week). Thus, the price of LNG exceeds the cost of the most expensive traditional bunker fuel by 609 USD: on November 14, the price of MGO LS in the port of Sines was quoted at 1107 USD/MT.

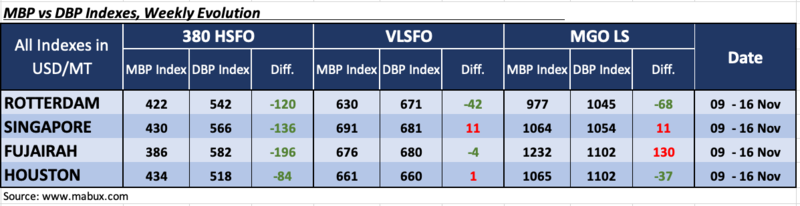

Over the week 46, the MDI Index (comparison of MABUX market bunker prices (MBP Index) vs MABUX digital bunker benchmark (DBP Index)) continued to register underestimation of 380 HSFO fuel grade in all four selected ports. The underprice margins moderately decreased and showed: in Rotterdam - minus $120, Singapore - minus $136, Fujairah - minus $196 and in Houston - minus $84.

In the VLSFO segment, according to MDI, Houston returned to the overpricing zone, joining Singapore: plus $1 and plus $11, respectively. Rotterdam remained undervalued by minus $42 and Fujairah - by minus $4. Undercharge premium declined slightly, while overcharge increased.

In the MGO LS segment, MDI registered fuel underpricing in two out of four selected ports: Rotterdam - minus $68 and Houston - minus $37. Singapore returned to the overpricing zone and joined Fujairah: plus $11 and plus $130 respectively. MDI Index did not have a firm trend in this bunker fuel segment.

The 4,251,000 metric tonnes (mt) of marine fuel sales in the Port of Singapore last month was the highest monthly total since October 2021. Last month’s overall total was bolstered by 2,154,300 mt of low sulphur fuel (LSFO) oil 380 cSt sales – the highest monthly total since January 2021. Sales of marine fuel oil (MFO) 380 cSt (1,309,700 mt) also reached a year-to-date high. Low sulphur marine gasoil (305,100 mt) saw also month-on-month decrease. During the first 10 months of the year a total of 39,372,500 mt of marine fuel was sold at the Port of Singapore – 5.3% down on the 41,589,400 mt registered during the same period in 2021.

International shipping association BIMCO has announced it has joined the Blue Visby Consortium which aims to support research into practical solutions that help reduce the shipping industry’s greenhouse gas (GHG) emissions. The Consortium works to mitigate ships' GHG emissions by about 15% through a multilateral platform named the Blue Visby Solution which optimises arrival times at their destinations by eradicating the practice of ‘Sail Fast then Wait’. The solution applies an algorithm to arrival times of groups of ships heading for the same destination, to give an optimal target arrival time for each ship while maintaining the scheduled arrival order. This is done by analysing a number of parameters, including the performance of each ship together with conditions such as weather and congestion at the destination.

The global bunker market is still in a phase of irregular changes looking for a sustainable trend.

By Sergey Ivanov, Director, MABUX

All news