The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

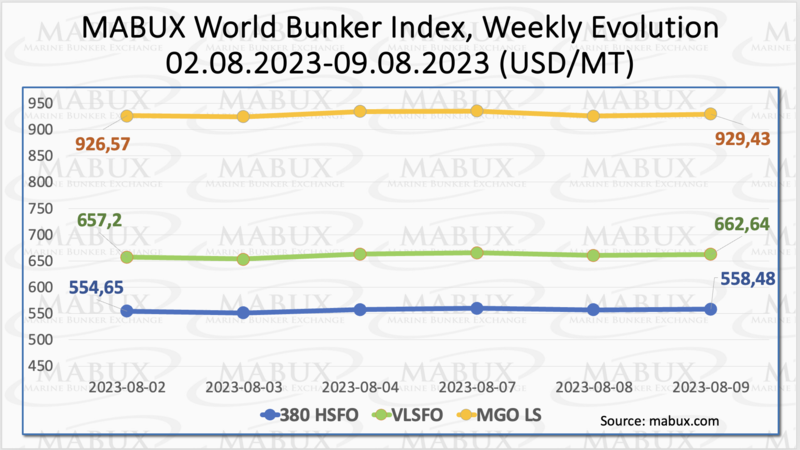

Over the Week 32, the MABUX global bunker indices showed relatively minor fluctuations, demonstrating moderate growth. The 380 HSFO index rose by 3.83 USD: from 554.65 USD/MT last week to 558.48 USD/MT. The VLSFO index added 5.44 USD (662.64 USD/MT versus 657.20 USD/MT last week). The MGO index also gained 2.86 USD (from 926.57 USD/MT last week to 929.43 USD/MT). At the time of writing, there was no sustainable trend in the market.

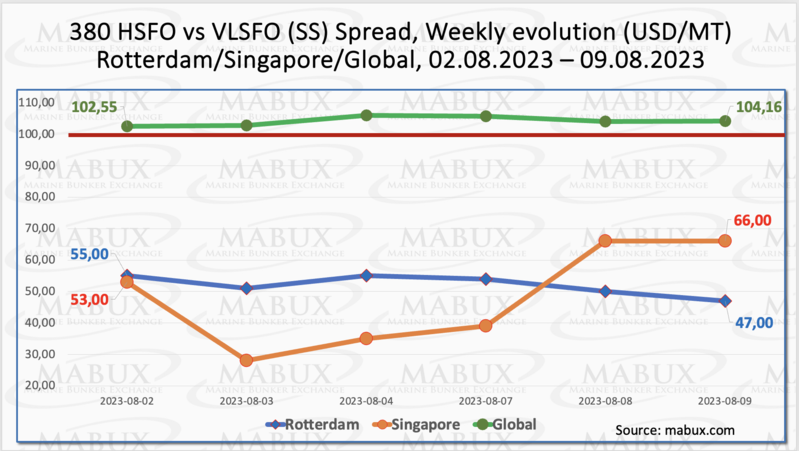

The Global Scrubber Spread (SS), which represents the price gap between 380 HSFO and VLSFO, exhibited minimal change, edging up by $1.61 to reach $104.16 compared to $102.55 the previous week. The weekly average, on the contrary, decreased by $1.70. In Rotterdam, the SS Spread dropped another $8 from $55.00 last week to $47.00, breaching $50 mark. The weekly average of the SS Spread in Rotterdam also continued to decline, dropping another $11.17. In Singapore, the price difference between 380 HSFO and VLSFO, on the contrary, increased by the end of the week: plus $13.00 ($66.00 vs. $53.00 last week). However, this index experienced a dip to $28 during the week. The weekly average for this spread decreased by $20.34. The noteworthy decline of SS Spread values below the $100 mark (considered SS breakeven) in the world's major ports continues to create a favorable scenario for low sulfur fuel VLSFO over the combination of HSFO and scrubbers. More information is available in the "Differentials" section of www.mabux.com.

European natural gas prices have surged more than 30% on Aug.08, as traders panicked over the possibility of reduced LNG supply from Australia, a world leading supplier of the commodity. The sudden jump was likely due to some traders rushing to close their short positions on the news of tightening supplies. Europe has failed to secure enough long-term LNG contracts to offset cut-off Russian gas imports, with some experts earlier predicting this may prove costly next winter and could sharply tighten the market.

Despite this, the price of LNG as bunker fuel in the port of Rotterdam showed a moderate decrease and reached 648 USD/MT on August 08 (minus 18 USD compared to the previous week). The price difference between LNG and conventional fuel as of August 08 increased to 232 USD in favor of LNG. On the same day, MGO LS was quoted at 880 USD/MT in the port of Rotterdam. More information is available in the LNG Bunkering section of www.mabux.com.

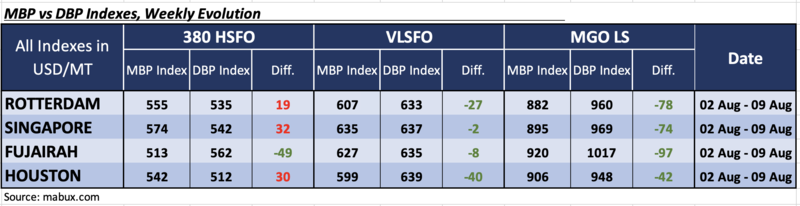

During Week 31, the MDI index (the ratio of market bunker prices (MABUX MBP Index) and the digital bunker standard MABUX (MABUX DBP Index)) noted a transition of certain ports into the overcharge zone, while the dominant trend of underpricing continued.

In the 380 HSFO segment, Fujairah remained the only underestimated port, where the average weekly underpricing decreased by 30 points. Rotterdam shifted into the overcharge zone, aligning with Singapore and Houston. The overpricing weekly average increased in Rotterdam by 18 points, in Singapore by 28 points, and in Houston by 21 points.

For the VLSFO segment, all four selected ports were in the underestimation zone. The average underpricing decreased by 17 points in Rotterdam, 14 points in Singapore, 18 points in Fujairah, and 2 points in Houston.

In the MGO LS segment, the MDI indicated a decline in average undercharge levels by 7 points in Rotterdam, 7 points in Singapore, and a significant 25 points in Fujairah. However, Houston experienced an 8-point increase in the average undercharge level.

Regarding the MGO LS segment, the average undervaluation reduced in Rotterdam by 7 points and in Houston by 9 points. In the other ports, MDI indicated growth, with a 3-point increase in Singapore and a 5-point increase in Fujairah.

For further information on the correlation between market prices and the MABUX digital benchmark, please refer to the "Digital Bunker Prices" section on www.mabux.com.

As per DNV, the order tally for methanol fuelled vessels in July was 48, beating LNG-fuelled ship orders for the third month in a row. In another record month for methanol, the order total included 15 retrofits. Orders for LNG-fuelled ships continue ‘at a steady pace’ with a total of 14 new vessels ordered last month. The class society also highlighted that July’s orders brought the number of confirmed LNG-fuelled crude oil tankers past the 100 mark, 65 of which are already in operation. The significant number of new confirmed orders and retrofits for methanol coincides with the delivery of the world’s first methanol fuelled container vessel and the signing of the first bunker supply agreement for green methanol for ships. According to DNV, as of July orders for methanol-fuelled vessels totalled 204, with 27 in operation and 177 on order. Containerships lead the pack in terms of vessel segment numbers, with 142 methanol-fuelled vessels on order. However, in the tanker segment there are already 23 vessels in operation, with 14 on order. To date, there are 949 confirmed orders for LNG-fuelled ships, with 420 of these already in operation. There are also 1,119 vessels with batteries installed, of which 800 are currently in operation.

As for the upcoming week, we expect the irregular changes to prevail while the market to be in the process of shaping a new distinct trend.

By Sergey Ivanov, Director, MABUX

All news