The joint review was contributed by IAA PortNews and the Institute of Natural Monopolies Research (IPEM)

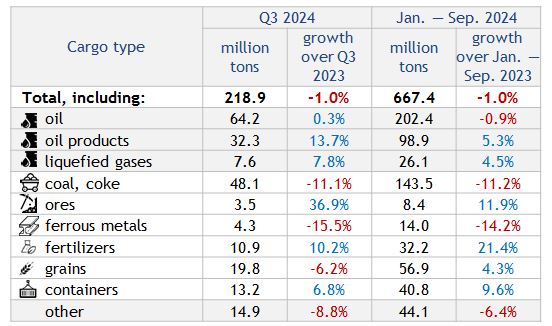

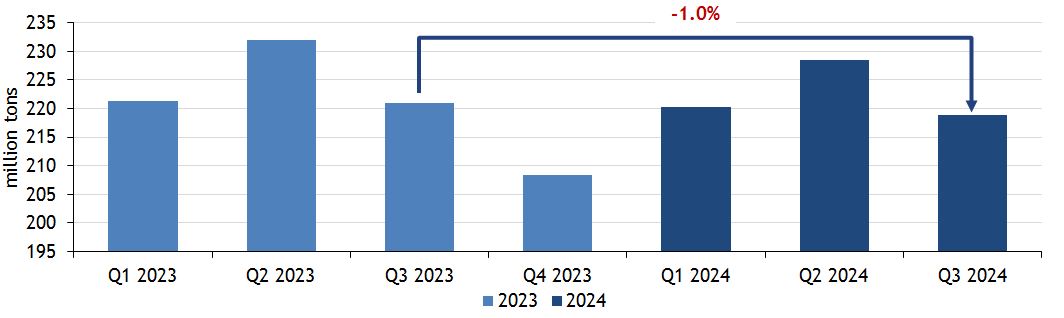

Russian seaports saw a downward trend in throughput in the third quarter of 2024: cargo volume fell by 1.0% on the same period a year earlier with decline recorded for the past four quarters in a row, the review showed.

The most noticeable decrease was recorded in the ferrous metals segment (-15.5%). This was attributed to a decline in prices and demand for metal products in China. Coal handling also dropped by 11.1% in the third quarter from the same period 2023. Infrastructure capabilities and the declining global prices were the main factors restraining the commodity exports. The limited capacity of the Baikal-Amur Mainline and Trans-Siberian Railway (RZD’s Eastern polygon) as well as rail access to the ports were among the infrastructure bottlenecks. Low coal prices in global markets make the product exports through the Azov-Black Sea and Arctic basins less profitable: the volume decline in those ports was more than 30% compared to the third quarter of 2023. The effect of the export duty on coking coal was an additional limiting factor.

Grain exports through the ports dropped by 6.2% for the first time this year. This is associated with a decrease in global market prices, a decline in exporters' margins and the suspension of wheat imports from Turkey.

However, crude oil exports edged up (+0.3%) after a long decline. This sustained growth is associated with Russia fulfilling its obligations under the OPEC+ agreement.

The seaports saw a 6.8-percent growth in container throughput in the third quarter. Liquefied gases and fertilizers volume also rose by 7.8% and 10.2%, respectively. The increase in liquefied gas exports is explained by lower reference base period of the third quarter, 2023 (when planned maintenance of plants was carried out) and the LNG production growth.

Russian and foreign liner services development encouraged container throughput growth. Fertilizer shipments increased thanks to the development of terminals in the Baltic Basin and the product exports from Belarus.

Oil product shipments increased by 13.7% in the third quarter, but the growth was due to the low base effects in July-Sept, 2023.

Volume of ore handled at the country’s seaports in July through September increased by 36.9% on the same period 2023.

Only the Baltic Basin seaports recorded a three-month volume gain (+12.9%), thanks to oil product shipments recovery and the fertilizer exports growth. The Far Eastern Basin terminals saw a 4.1-percent throughput decline attributed to challenges in coal exports. The Azov-Black Sea and Arctic basin ports also reported volumes decrease (-6.6%, -7.9%, respectively) due to a decline in shipping coal, as well as crude oil on the longest routes. Grain cargo traffic contributed to the largest throughput decrease seen in the Caspian Basin ports (-15.2%).

Russian seaports container throughput increased by 7.8% in TEU compared to the same period 2023 with sustainable upward trend seen in all port basins. In general, volume growth continues in Russia, but its rate has been declining for the fourth quarter in a row. This trend is typical for the Baltic and Azov-Black Sea basins (growth +14.1% and +1.7%, respectively). On the contrary, in the Arctic and Far Eastern basins volume growth is accelerating (+54.3% and +4%, respectively). In the Caspian Basin, container traffic showed growth (+15.5%) for the first time since the Q2, 2023.

Infographics document is available here >>>>

When using the review materials, reference to the joint project of IPEM and PortNews is required