The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

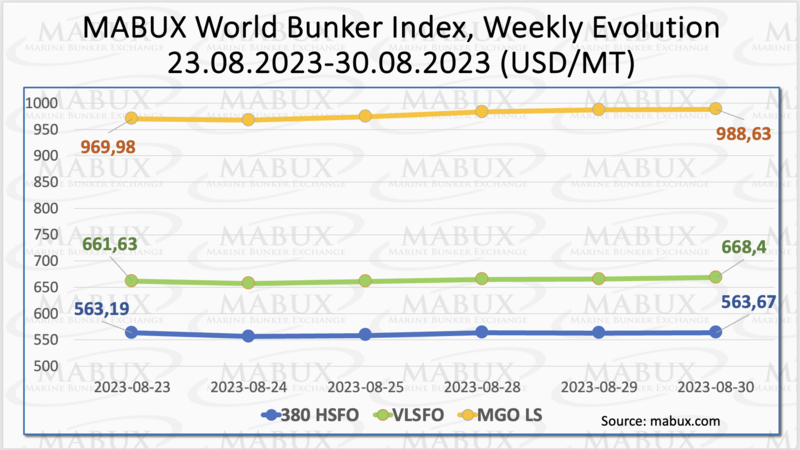

During the Week 35, the MABUX global bunker indices showed a slight upward movement. The 380 HSFO index saw a nominal increase of 0.48 USD, rising from 563.19 USD/MT the previous week to 563.67 USD/MT. The VLSFO index experienced a more significant rise of 6.77 USD, moving from 661.63 USD/MT to 668.40 USD/MT. The MGO index exhibited a substantial surge of 18.65 USD, jumping from 968.98 USD/MT to 988.63 USD/MT. At the time of writing, the market was experiencing a moderate upward trend.

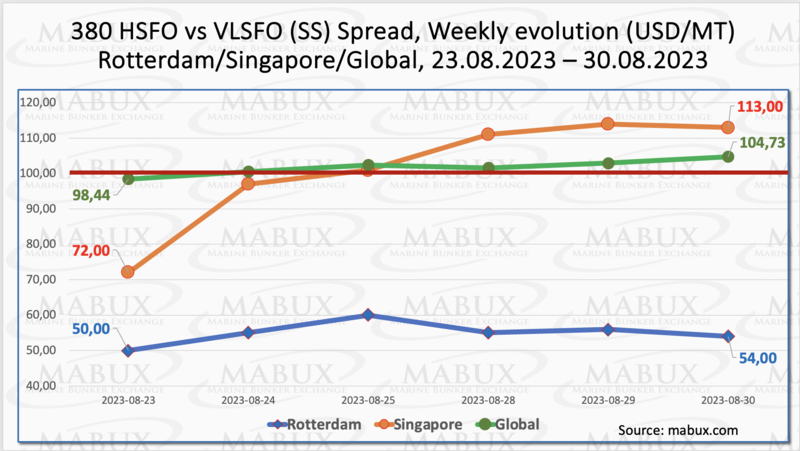

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - showed a moderate growth: plus $6.29 ($98.44 versus $104.73 last week, breaching the 100.00 USD mark (SS breakeven). The average weekly value, on the contrary, decreased by $1.94. In Rotterdam, SS Spread continued to rise, adding $4.00 from $50.00 last week to $54.00. The weekly average of SS Spread in Rotterdam also increased by $10.00. In Singapore, the price difference between 380 HSFO and VLSFO showed the most significant increase: surging by 41.00 USD (113.00 USD compared to 72.00 USD last week), confidently exceeding the 100 USD mark. The weekly average also rose by $27.50. It is expected that the SS Spread will continue moderate gains in the upcoming week. More information is available in the "Differentials" section of www.mabux.com.

Based on data from Global Witness, the European Union has experienced a substantial 40% increase in its imports of liquefied natural gas (LNG) from Russia during the period of January to July 2023, in comparison to the corresponding timeframe in 2021. This growth is attributed to the absence of any bans or sanctions on Russian gas within Europe. Notably, Spain has ascended to the position of the second-largest global purchaser of Russian LNG, closely pursued by Belgium. Preceding these two European Union member states is China, which accounted for 20% of Russia’s total LNG exports during the initial seven months of 2023. Spain contributed to 18% of Russia’s overall LNG exports, while Belgium acquired 17%. In the same period of 2021, Spain and Belgium ranked fifth and seventh, respectively, among the principal buyers of Russian LNG. Overall, the EU bought 52% of Russia’s LNG exports between January and July 2023, compared to 49% in 2022 and 39% in 2021.

On August 28, the cost of LNG as bunker fuel at the port of Sines, Portugal dropped, reaching 820 USD/MT. This marked a decrease of 79 USD in comparison to the previous week's price. Notably, the price difference between LNG and conventional fuel on August 28 witnessed a significant expansion, favoring LNG by 185 USD. On the same day, MGO LS was quoted at 1005 USD/MT at the port of Sines. More information is available in the LNG Bunkering section of www.mabux.com.

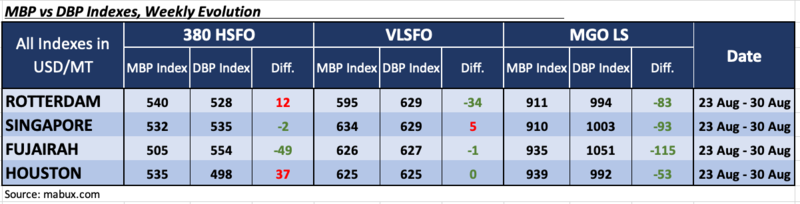

During Week 35, the MDI index (the ratio of market bunker prices (MABUX MBP Index) and the digital bunker benchmark MABUX (MABUX DBP Index)) showed that the underpricing trend continued to dominate the global bunker market across all bunker fuel segments.

In the 380 HSFO segment, Singapore entered the undervaluation zone, joining Fujairah, while the average weekly underpricing increased by 31 and 7 points, respectively. In the other two ports: Rotterdam and Houston, the MDI index registered an overestimation. The average weekly overcharge fell by 14 points in Rotterdam but rose by 10 points in Houston.

For the VLSFO segment, the MDI index indicated that only Singapore was in the overvaluation zone, with its average level decreasing by 3 points. Rotterdam and Fujairah continued to be undervalued. The undervaluation’s weekly average in Rotterdam increased by 5 points, while it remained unchanged in Fujairah. In Houston, MDI recorded a 100 percent correlation between market prices and the digital benchmark.

Within the MGO LS segment, all selected ports remained undervalued. The average weekly underpricing widened in Rotterdam by 5 points, in Singapore by 6 points, in Fujairah by 16 points, and in Houston by 18 points.

For further information on the correlation between market prices and the MABUX digital benchmark, please refer to the "Digital Bunker Prices" section on www.mabux.com.

In its recently published Global Outlook, ExxonMobil has presented a projection indicating that global CO2 emissions related to energy will diminish by 25% by 2050, owing to the expansion of lower-emission alternatives. Nevertheless, oil and natural gas are poised to continue fulfilling a significant share (54%) of the world's energy requirements and will retain their "essential" role in maritime shipping. ExxonMobil's forecast also envisions an unprecedented surge in the adoption of lower-emission alternatives, with wind and solar energy contributing 11% of the global energy supply by 2050 – a substantial five-fold increase compared to their current contribution. Additional lower-emission options, including biofuels, carbon capture and storage, hydrogen, and nuclear power, will also assume pivotal roles. ExxonMobil further acknowledges that while the utilization of oil is expected to notably decrease in personal transportation, as the prevalence of electric cars continues to rise, its significance will endure in industrial processes and heavy-duty transportation sectors like shipping, long-distance trucking, and aviation. Despite that, fossil fuels remain the most effective way to produce the massive amounts of energy needed to create and support the manufacturing, commercial transportation, and industrial sectors that drive modern economies. For this reason, a critical goal of any energy transition will be the affordable decarbonisation of these economic sectors that account for half of all energy-related emissions.

We expect that next week the global bunker market will be dominated by a moderate upward evolution.

By Sergey Ivanov, Director, MABUX