The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

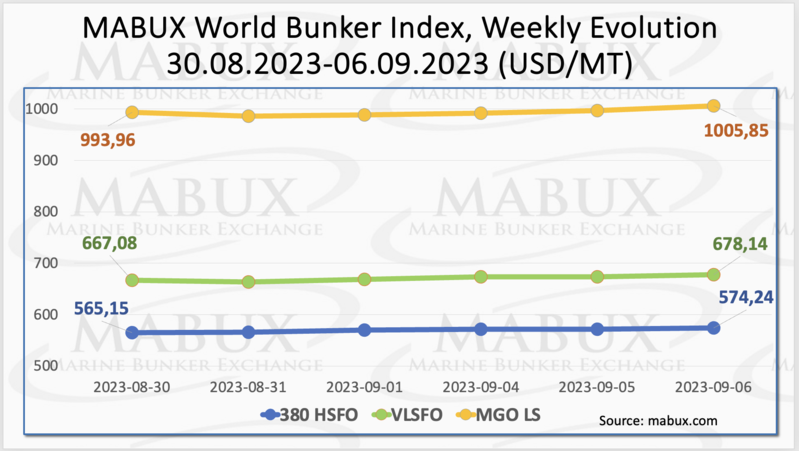

Over the Week 36, the MABUX global bunker indices continued trending upwards. The 380 HSFO index rose by 9.09 USD: from 565.15 USD/MT last week to 574.24 USD/MT. The VLSFO index, in turn, increased by 11.06 USD (678.14 USD/MT versus 667.08 USD/MT last week). The MGO index added 11.89 USD (from 993.96 USD/MT last week to 1005.85 USD/MT), surpassing the 1000 USD mark for the first time since February 03, 2023. At the time of writing, bunker indices continued uptrend evolution.

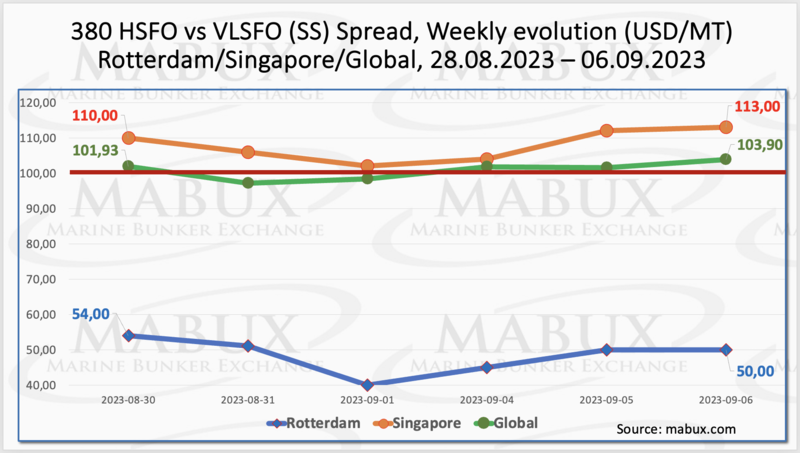

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO – widened slightly over the week: plus $1.97 ($103.90 vs. $101.93 last week), but still remaining close to the $100.00 mark, which signifies SS breakeven. The weekly average, on the contrary, decreased by $0.97. In Rotterdam, SS Spread resumed its decline, dropping by $4.00: from $54.00 last week to $50.00, even falling to $40.00 on September 01. The average weekly SS Spread in Rotterdam also decreased by $6.67. In Singapore, the price difference between 380 HSFO and VLSFO showed a slight increase of $3.00 ($113.00 vs. $110.00 last week), staying above the $100.00 mark. The weekly average also rose by $6.50. We expect SS Spread do not show a sustainable trend in the upcoming week. More information is available in the "Differentials" section of www.mabux.com.

European gas prices experienced a surge earlier this month due to potential industrial action threats by workers at three LNG facilities in Australia. While strikes were averted at one facility, the risk persisted at the other two, effectively maintaining a floor for gas prices. In the meantime, Europe's gas storage levels are higher than typical for this time of year, primarily attributable to the retention of volumes from the previous year, which had been bought at record-high prices. It made no sense to resell them at a huge loss, while the continent’s storage is now 92.5% full. This surplus could serve as a comfortable buffer in the event of an outage, particularly if the outage proves to be of short duration.

Despite the momentary growth of gas indexes, the price of LNG as bunker fuel at the port of Sines (Portugal) showed another decrease, reaching 758 USD/MT on September 04 (minus 62 USD compared to the previous week). At the same time, the difference in price between LNG and conventional fuel as of September 4 also continued to expand: 220 USD in favor of LNG: in the port of Sines, MGO LS was quoted that day at 978 USD/MT. More information is available in the LNG Bunkering section of www.mabux.com

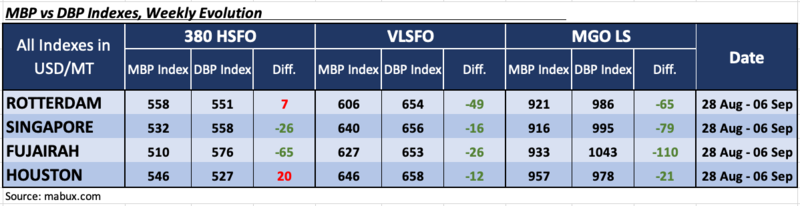

During Week 36, the MDI index (the ratio of market bunker prices (MABUX MBP Index) and the digital bunker benchmark MABUX (MABUX DBP Index)) showed that the trend of underestimating bunker fuel still prevails in the global bunker market.

In the 380 HSFO segment, Singapore and Fujairah remained in the underestimation zone, with the average weekly underpricing increasing by 24 and 16 points, respectively. In the other two ports: Rotterdam and Houston, the MDI registered an overcharging. The average weekly overpricing ratio fell by 5 points in Rotterdam and by 17 points in Houston.

For the VLSFO segment, according to the MDI index, Singapore has moved into the underprice zone. Thus, all four selected ports were underestimated. The average undercharge index rose by 15 points in Rotterdam, 21 points in Singapore, 25 points in Fujairah and 12 points in Houston.

In the MGO LS segment, all selected ports remained undervalued, while the average undervaluation declining by 18 points in Rotterdam, 14 points in Singapore, 5 points in Fujairah and 32 points in Houston.

For more details on the correlation between market prices and the MABUX digital benchmark, please refer to the "Digital Bunker Prices" section on www.mabux.com.

Wood Mackenzie said that Asian LNG buyers are navigating a near-term market that is ‘so finely balanced that any supply disruptions or demand upsides could cause significant price volatility’. According to Wood Mackenzie data, Australia and Qatar will be the biggest suppliers of LNG to Asia throughout 2023-2030, with volumes of over 886 million tonnes and 827 million tonnes respectively. This will account for almost 60% of the total volumes of LNG delivered into Asia during this period. With the new wave of LNG projects not expected to make a significant impact in terms of increased supply until 2026, the market looks set to remain tight. Wood Mackenzie data shows LNG year-on-year supply growth averaging 40 million metric tonnes per annum (mmtpa) annually from 2026 to 2028, helping the global market to rebalance, which is predicted to bring prices down. It is expected that this will improve gas affordability, facilitate LNG availability for Europe and enable a rebound of demand in Asia.

We expect the global bunker market to maintain the potential for further moderate growth in the coming week.

By Sergey Ivanov, Director, MABUX

All news