The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

Last week ended with the largest one-day drop in crude oil prices since April 2020, as markets reacted to the discovery of the new Omicron coronavirus variant and the introduction of a raft of travel restrictions. Marine fuel prices followed the crude market and experienced significant decline. While uncertainty remains about the potential impact of Omicron on international travel and global trade, there are some signs that the initial reaction to the new variant may have been overly pessimistic.

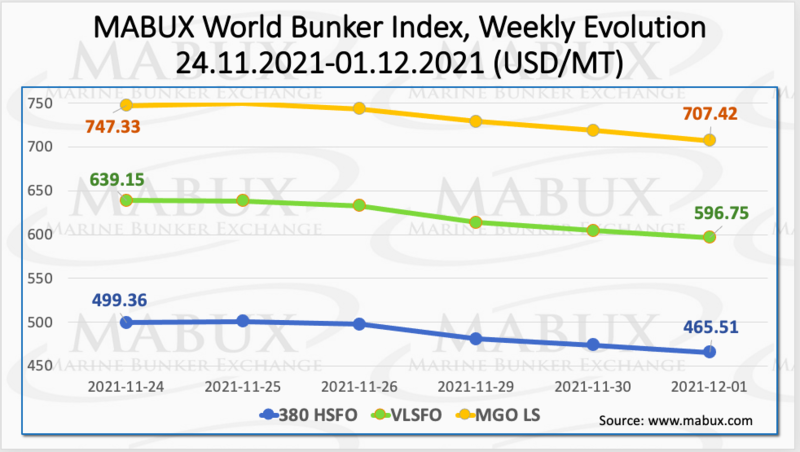

On a Week 48, the MABUX World Bunker Index showed a sharp decline in the main grades of bunker fuels. The 380 HSFO Index dropped by 33.85 USD: from 499.36 USD / MT to 465.51 USD / MT. The VLSFO index lost 42.40 USD: from 639.15 USD / MT to 596.75 USD / MT, while the MGO index decreased by 39.91 USD (from 747.33 USD / MT to 707.42 USD / MT).

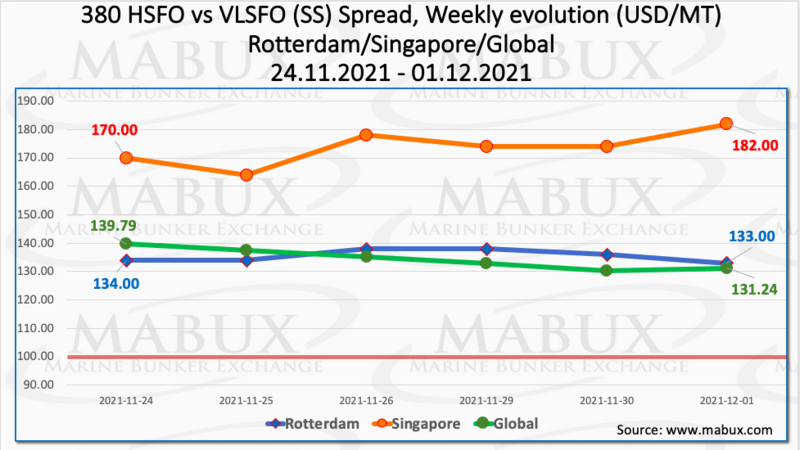

Despite the sharp drop of bunker prices, the weekly average Global Scrubber Spread (SS) - the difference in price between the 380 HSFO and VLSFO - remained virtually unchanged over the week, just $ 1.15 down ($ 134.51 versus $ 135.66 last week). Meanwhile, the average SS Spread in Rotterdam rose to $ 135.50 vs. $ 133.33 (plus $ 2.17). However, the most significant change was the growth of the SS Spread average in Singapore by $ 15.84 to $ 173.67 ($ 157.83 last week). Sharp price fluctuations observed in the bunker market over the past week, hampered the formation of a firm SS Spread trend. More information is available in the Differentials section of the www.mabux.com.

Gas indexes continued to rise on a week: Europe anticipates a cold start of December, higher withdrawals from the storage, while gas supply is tight. On December 01, another increase of LNG bunker prices was recorded at the port of Risavika (Norway) to 1775.37 USD / MT (versus 1592.67 USD / MT a week ago). The current price of LNG in Risavika is 1144 USD up the price of MGO LS in Bergen (631 USD / MT as of November 26). At the same time, the LNG bunker price at the port of Sines (Portugal) jumped on December 01 to 2396 USD / MT (versus 2050 USD / MT a week ago). Here, the current price of LNG is 1701 USD higher than the price of MGO LS - a record premium in 2021.

The volatility in the global bunker market also affected the correlation differences between the MABUX MBP Index (market bunker prices) and the MABUX DBP Index (MABUX digital bunker benchmark) in the four global largest hubs over the past week. In particular, 380 HSFO grade was underestimated in three out of four ports: in Rotterdam - minus $ 11, in Singapore - minus $ 6 and in Fujairah - minus $ 1. Houston remains the only port where the MABUX MBP / DBP Index registered an overpricing by $ 35.

VLSFO fuel grade, according to the MABUX MBP / DBP Index, came over to the overcharge segment for all ports: plus $ 9 in Rotterdam, plus $ 56 in Singapore, plus $ 52 in Fujairah and plus $ 30 in Houston. While in Singapore and Fujairah, the overpricing ratio increased by 19 points for each port, in Houston the Index added 29 points at once.

As for the MGO LS, the MABUX MBP / DBP Index has registered an overcharge of this fuel grade in two out of four selected ports: in Fujairah - plus $ 31 and in Houston - plus $ 22. In all other ports, MGO LS grade was underestimated: in Rotterdam - minus $ 44 and in Singapore - minus $ 11. The most significant change was the increase of overcharge margin in Houston by $ 23.

Negotiations at last week’s hybrid meeting of the Marine Environment Protection Committee (MEPC 77) have indicated support for zero emission shipping by 2050 – a more ambitious proposition than the IMO’s current 50% GHG emissions reduction goal – but discussions on the IMO's $5 billion R&D fund as well as the use of market-based measures, which are seen by many industry stakeholders as a way of accelerating shipping’s energy transition, have now been moved onto the agenda of the Intersessional Working Group on Reduction of GHG Emissions from Ships which will meet in 2022. A number of countries vetoed both the 2050 zero emission target and the resolution, including Brazil China, Russia, Saudi Arabia and the United Arab Emirates. Meanwhile, one of the top questions was he introduction of a carbon levy on bunker fuel. Countries that were in favour of a carbon levy – either as a standalone measure or as part of a basket of measures – included the EU27, Canada, Japan, Liberia and Pacific Islands nations. However, opposition to this came from a number of countries, including Saudi Arabia, Brazil, Argentina, China and Russia.

Source: www.mabux.com

All news