The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

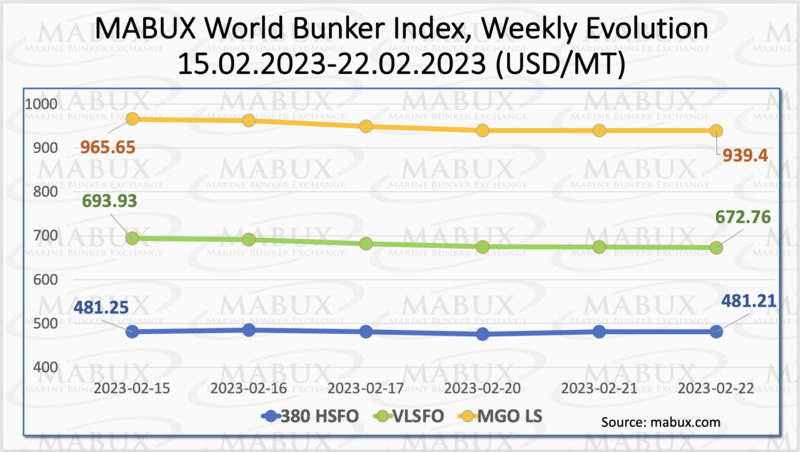

Over the Week 08, MABUX global bunker indices showed a moderate decline. The 380 HSFO index decreased by symbolic 0.04 USD: from 481.25 USD/MT last week to 481.21 USD/MT. The VLSFO index, in turn, fell by 21.17 USD (672.76 USD/MT versus 693.93 USD/MT last week). The MGO index also lost minus 26.25 USD (from 965.65 USD/MT last week to 939.40 USD/MT). At the time of writing, irregular fluctuations prevailed in the market.

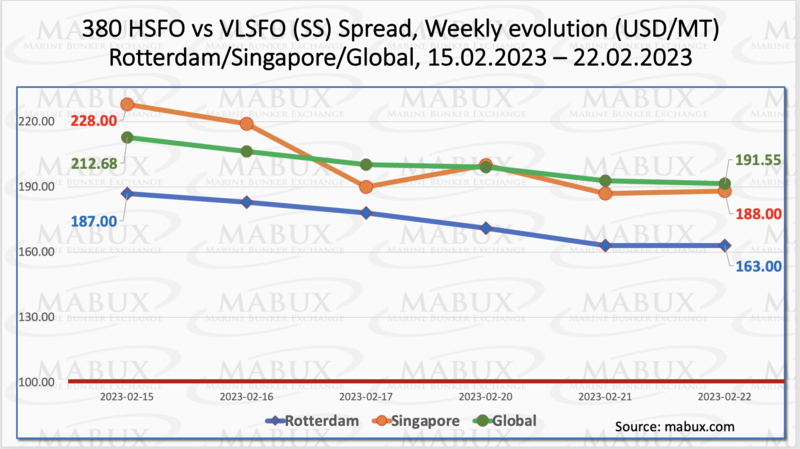

The Global Scrubber Spread (SS) - the price differential between 380 HSFO and VLSFO - showed a firm decline for Week 08 - minus $ 21.13 ($ 191.55 vs. $ 212.86 last week), breaking the psychological mark of $ 200. Meantime, the Global average also decreased by $15.14. In Rotterdam, SS Spread fell by $15.16 to $163.00 (vs. $187.00 last week). In Singapore, the 380 HSFO/VLSFO price difference showed again the most significant reduction: minus $40, falling to $188 and breaking the $200 mark. The SS Spread weekly averages in Rotterdam and Singapore also decreased by $15.16 and $46.17, respectively. Next week, we expect the SS Spread to continue downward trend. More information is available in the "Differentials" section of www.mabux.com.

Europe’s benchmark natural gas price fell this week to the lowest level in 18 months as concerns about a gas crisis this winter continue to recede amid mild weather and above-average inventories across the continent. But the falling price in Europe could invoke more demand in the industrial sector, as well as more demand in Asia, which would compete for spot LNG supply with Europe.

The price of LNG as a bunker fuel in the ARA region declined slightly and reached 969 USD/MT on February 21 (minus 11 USD compared to the previous week). The difference in price between LNG and conventional fuel on February 21 was 189 USD: MGO LS in the ARA region was quoted at 780 USD/MT that day. The price difference continues to gradually decrease. We expect this trend to continue. More information is available in the “LNG Bunkering” section at www.mabux.com.

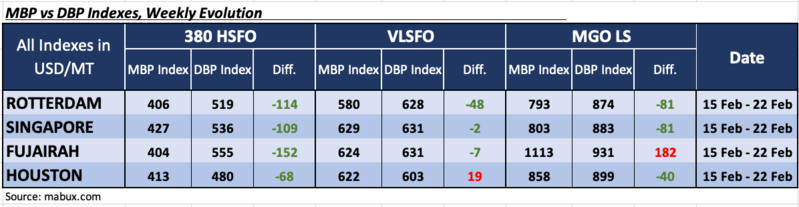

Over the Week 08, the MDI index (correlation of MABUX market bunker prices (MBP Index) vs MABUX digital bunker benchmark (DBP Index)) registered underestimation of 380 HSFO in all four selected ports. The average underestimation margins decreased moderately and amounted to: Rotterdam – minus $114, Singapore - minus $109, Fujairah - minus $152 and Houston - minus $68.

In the VLSFO segment, according to MDI, two ports at once: Singapore and Fujairah have moved into the underestimation zone and joined Rotterdam. The underprice margins were minus $2, minus $7 and minus $48, respectively. Houston remained the only overvalued port in this fuel segment with a plus $19. In general, there is a gradual approach of market prices and the MABUX digital benchmark to 100-percent correlation.

In the MGO LS segment, Houston moved into the undervalued zone and joined Rotterdam and Singapore. The undercharge ratio was minus $40, minus $81 and minus $81, respectively. Fujairah remained the only overvalued port, plus $182. The most significant change in this bunker fuel segment was an increase of undercharge average in Houston by 43 points.

More information on the correlation between market prices and MABUX digital benchmark is available in the “Digital Bunker Prices” section at www.mabux.com.

Bunker sales in Panama slipped from 476,109 metric tonnes (mt) in December to 434,807 mt in January. Last month’s total also represents a 3.7% year-on-year decrease on the 451,664 mt registered in January 2022.Some 308,271 mt of very low sulphur were sold last month. This was 11.1% down on the 346,797 mt recorded in December and 5% down on the 324,456 mt recorded in January 2022. High sulphur fuel oil sales (78,767 mt) rose 6.7% month-on-month (m-o-m) but fell 1.4% on the year. Elsewhere, sales of low sulphur marine gasoil slipped from 40,459 mt in December to 36,218 mt in January; and marine gasoil also fell, from 15,012 mt to 11,551 mt. As previously reported, Panama saw a 4.3% increase in bunker fuel sales in 2022.

Uptrend forecasts of bunker prices due to the EU embargo on imports of refined petroleum products from Russia implemented on February 05 did not materialize: indices are declining moderately. We expect this trend to continue next week.

By Sergey Ivanov, Director, MABUX