The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

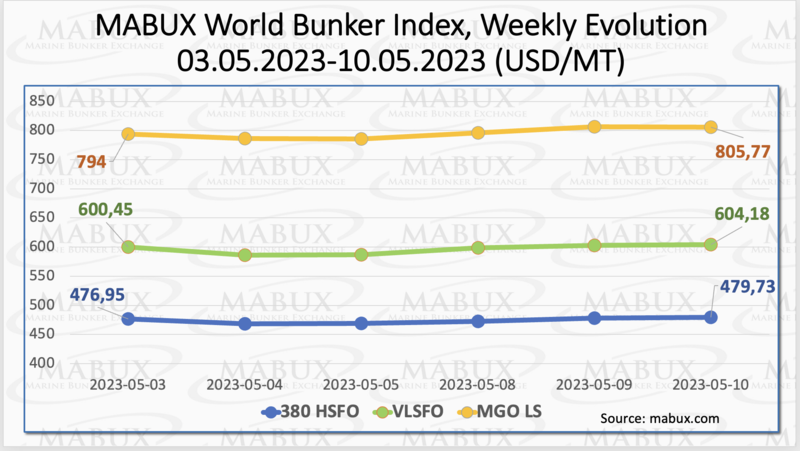

Over Week 19, the global MABUX bunker indices showed a moderate upward correction. The 380 HSFO index increased by 2.78 USD, rising from 476.95 USD/MT in the previous week to 479.73 USD/MT, but it remained below the 500 USD mark. The VLSFO index also went up by 3.73 USD, from 600.45 USD/MT last week to 604.18 USD/MT. The MGO index showed an increase of 11.77 USD, from 794.00 USD/MT in the previous week to 805.77 USD/MT. As of the time of writing, the market did not exhibit a firm trend.

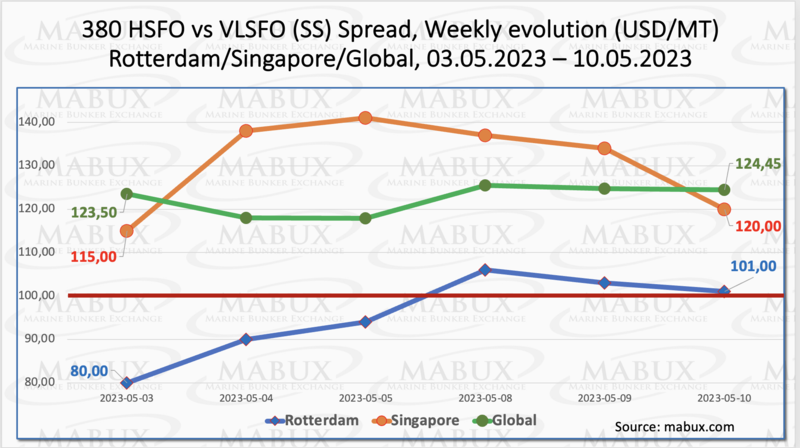

During Week 19, the Global Scrubber Spread (SS) - the difference in price between 380 HSFO and VLSFO - remained largely stable, with a minor increase of $0.95 ($124.45 compared to $123.50 in the previous week). However, the weekly average SS Spread decreased by $1.46. In Rotterdam, the SS Spread saw a rise of $21, surpassing the psychological $100 mark once again, while the weekly average of SS Spread in Rotterdam also rose by $6.00. In Singapore, the 380 HSFO/VLSFO price difference added $5.00 over the week ($120 compared to $115.00 last week), and the average weekly value increased by $11.66. Overall, signs of some upward correction were observed this week, marking the first time in the last 7 weeks. For further details, please refer to the Differentials section of www.mabux.com.

Europe’s benchmark natural gas prices extended losses this week - a sixth week of declines amid comfortable inventories and tepid gas demand in Europe and Asia. Spot LNG prices for delivery into north Asia in June have also slumped – to the lowest level in two years, as demand for the refilling of inventories in top buyers China, Japan, and South Korea remains weak.

The price of LNG as bunker fuel in the port of Sines (Portugal) decreased again on May 08 to 933 USD/MT (minus 52 USD compared to the previous week). The price difference between LNG and conventional fuel also decreased to 183 USD on May 08: MGO LS in the port of Sines was quoted at 750 USD/MT that day. The market continues to register a gradual reduction in the difference of prices between LNG and conventional fuel. More information is available in the LNG Bunkering section of www.mabux.com.

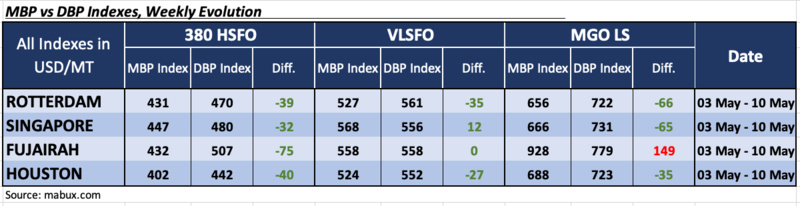

In Week 19, the MDI index (the ratio of market bunker prices (MABUX MBP Index) and the MABUX digital bunker benchmark (MABUX DBP Index)) indicated that 380 HSFO fuel continued to be undervalued in all four selected ports. The average weekly underprice levels showed moderate declines in all ports, ranging from minus $4 to minus $11, except for Houston, where the MDI increased by 10 points.

Similarly, in the VLSFO segment, the fuel continued to be undervalued in all selected ports, with slight declines in undervaluation margins in Rotterdam and Houston by $14 and $3, respectively. However, in Singapore, the MDI rose by $12, while in Fujairah, there was a 100 percent correlation between the market price and the digital benchmark, indicating that the fuel was neither undervalued nor overvalued.

Regarding the MGO LS segment, three ports - Rotterdam, Singapore, and Houston - still showed underestimation. The average weekly of undercharge for all three ports remained almost unchanged. Fujairah is still the only overvalued port - plus $149.

For more detailed information on the correlation between market prices and the MABUX digital bunker benchmark, please refer to the "Digital Bunker Prices" section at www.mabux.com.

According to DNV, oil demand in the transport sector is forecast to halve by 2050 and the fuel mix in the maritime sector will ‘likely transition from being almost entirely oil-based to an energy mix comprising of 50% low- and zero-carbon fuels, 19% natural gas and 18% biomass. However, DNV warned that ‘the present pace of the transition still falls severely short of the goals of the Paris Agreement’, so ‘opportunities to accelerate change through pilot projects and uptake of alternative energy need to be seized as soon as possible’. Even though the combined emissions from shipping, aviation and road transport are predicted to almost halve by 2050, DNV is forecasting that their contribution to overall emissions will increase from around 25% to 30%. DNV also said, that there is a pressing need for reliable non-fossil fuels to support emission reductions, particularly in the maritime and aviation sectors. It is essential that policy makers accelerate efforts to incentivise research and development, pilot projects and commercial uptake of carbon-neutral and zero-carbon fuels across the transport sector to support mid-century net zero goals.’

Multidirectional dynamics continue to prevail in the global bunker market, and we anticipate that there will be no a sustainable trend in bunker indices in the coming week.

By Sergey Ivanov, Director, MABUX

All news