The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

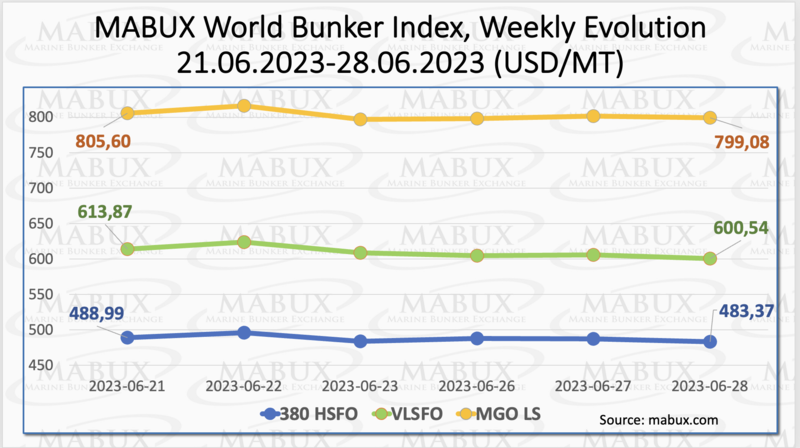

As of the 26th week, the global MABUX bunker indices experienced a moderate decline. The 380 HSFO index witnessed a decrease of 5.62 USD, dropping from 488.99 USD/MT in the previous week to 483.37 USD/MT, remaining well below the 500 USD threshold. Similarly, the VLSFO index declined by 13.33 USD, reaching 600.54 USD/MT compared to 613.87 USD/MT last week, thereby hitting the level of 600 USD. The MGO index also saw a decrease of 6.52 USD, falling from 805.60 USD/MT in the previous week to 799.08 USD/MT, once again dipping below the 800 USD mark. At the time of writing, the market was in a downtrend.

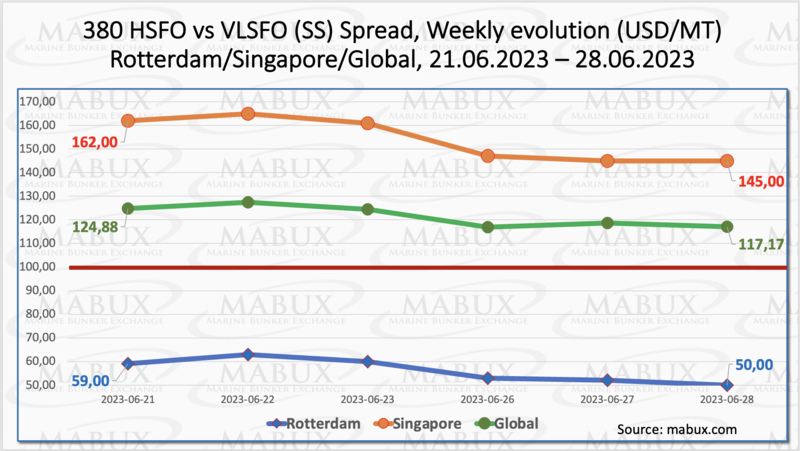

The Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - continued a notable decline dropping by $7.71 ($117.17 compared to $124.88 last week). The weekly average also decreased by $1.51. In Rotterdam, the SS Spread fell by $9.00, reaching $50.00, its lowest value since November 13, 2020. The weekly average of SS Spread in Rotterdam also saw a decline of $9.50. Similarly, in Singapore, the price difference between 380 HSFO and VLSFO decreased by $17.00 over the week ($145 compared to $162.00 last week), and the weekly average dropped by $3.50. This continuous significant reduction in the SS Spread in Northern Europe creates favorable conditions for the growth of LNG bunkering operations. For more detailed information, please refer to the Differentials section of www.mabux.com.

Europe’s LNG imports rose last year to levels that surpassed its imports of natural gas via pipeline, The Energy Institute’s data shows that Europe’s natural gas imports via pipeline in 2022 were 35% lower than the previous year, coming in at 150.8 bcm—most of which still came from Russia. Meanwhile, Europe’s LNG imports rose to more than 170 bcm. To achieve this level of LNG imports, Europe had to construct import terminals for LNG. Norway is now the single-largest gas supplier to Europe.

There has been a slight increase in the price of LNG as bunker fuel at the port of Sines in Portugal.As of June 26, the price stood at 825 USD/MT, marking a drop of 16 USD compared to the previous week. Consequently, the price differential between LNG and conventional fuel on June 26 favored marine gas oil (MGO), with MGO being quoted at 783 USD/MT in the port of Sines (42 USD lower than LNG). More information is available in the LNG Bunkering section of www.mabux.com.

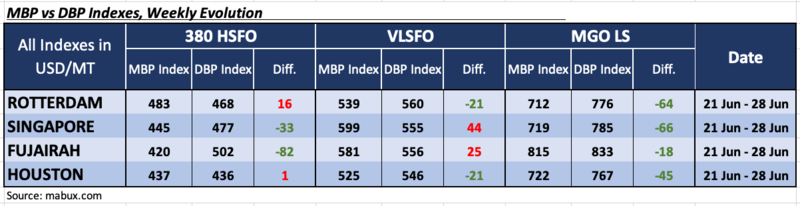

During week 26, the MDI index (the ratio of market bunker prices (MBP Index) and MABUX digital bunker benchmark (DBP Index)) registered an underpricing of 380 HSFO fuel in two out of the four selected ports: Singapore and Fujairah. The underestimation weekly averages decreased in the range from 2 to 6 points. Houston moved into the fuel overpricing zone and joined Rotterdam. The average overcharge ratio increased by 3 to10 points.

In the VLSFO segment, based on MDI data, Singapore and Fujairah remained overvalued ports. The average overprice margins increased by 3 to 6 points. Rotterdam and Houston, on the other hand, were in the underpricing zone, with no change in the average undercharge levels for both ports.

In the MGO LS segment, MDI registered underestimation in all four selected ports. The average undervaluation levels rose in Singapore and Fujairah by $2 and $13, respectively, while they decreased by $8 in Rotterdam and $1 in Houston.

More information on the correlation between market prices and MABUX digital bunker benchmark is available in "Digital Bunker Prices" section on www.mabux.com.

A new report published by class society DNV notes that if shipping was to achieve full decarbonisation by 2050 primarily by using biofuels, in combination with energy efficiency measures, some 250 million tonnes of oil equivalent (Mtoe) of biofuels would be needed. According to the report, the use of biofuel as a bunker fuel has, up until very recently, been extremely low. However, in 2022 its uptake began to accelerate, with reports of around 930,000 tonnes of blended biofuel being bunkered in Singapore and Rotterdam. It still accounts for just 0.1% of total maritime fuel consumption of 280 million tonnes of oil equivalent (Mtoe) per year. The DNV database has identified around 5,000 biofuel production facilities worldwide. According to the report, global production of advanced biofuels stands at 11 Mtoe per year in 2023 but these volumes will increase to 23 Mtoe per year by 2026. By 2050, the supply of biofuels could hit 500-1,300 Mtoe per year, which means that shipping would require between 20% and 50% of this supply if it was to decarbonise primarily by using biofuels. The report concludes that it is likely that biofuels will play an important role in shipping over the coming decades, limits on production capacity and competition from other industry sectors, mean that biofuels cannot be shipping’s only solution to decarbonisation.

We anticipate relatively stable conditions in the global bunker market for the upcoming week. However, there is a possibility of moderate upward corrections in bunker indices.

By Sergey Ivanov, Director, MABUX

All news