The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

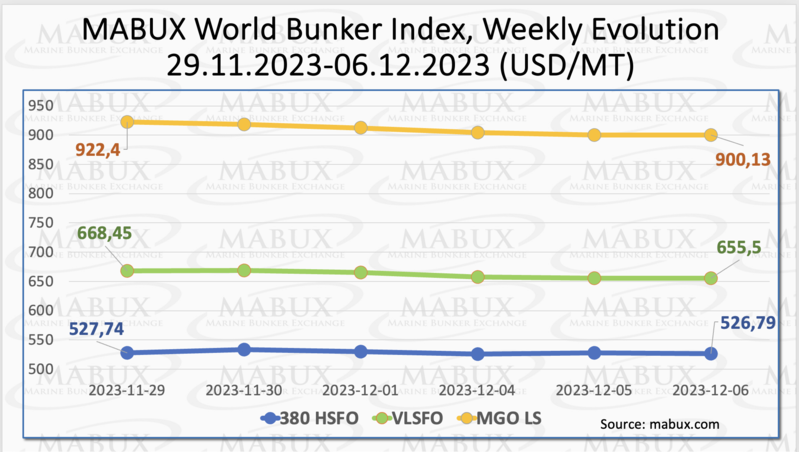

During Week 49, the MABUX global bunker indices continued moderate downward trend. The 380 HSFO index saw a nominal decrease of 0.95 USD, moving from 527.74 USD/MT to 526.79 USD/MT. Despite this decline, it remained above the 500 USD threshold. The VLSFO index dropped by 12.95 USD (655.50 USD/MT compared to 668.45 USD/MT last week), while the MGO index fell by 22.27 USD (from 922.40 USD/MT to 900.13 USD/MT). At the time of writing, there was no clear trend in the market.

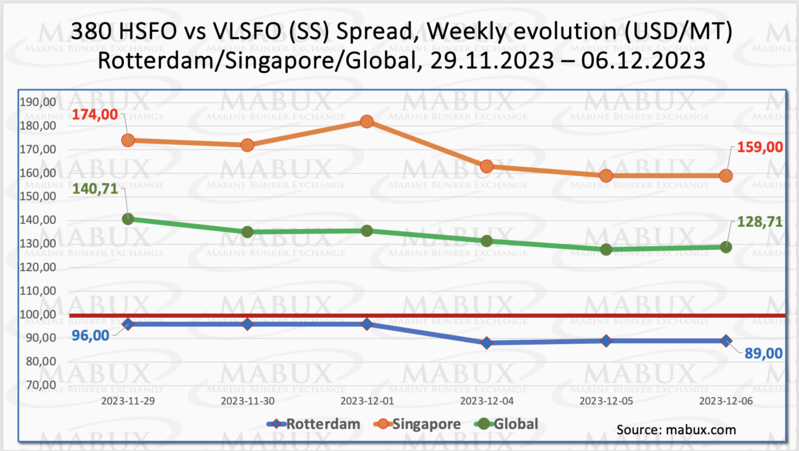

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - showed a further reduction: minus $12.00 ($128.71 versus $140.71 last week), still remaining above the critical $100.00 mark (SS breakeven). The weekly average also decreased by $8.23. In Rotterdam, SS Spread fell by $7 to $89 by the end of the week, consistently staying below the $100 mark, with the weekly average also decreasing by $8.23. Singapore experienced the most significant drop in the 380 HSFO/VLSFO price difference, recording minus $15 (159.00 USD versus 174.00 USD last week), while the weekly average decreasing by $47.50. We expect the sustainable narrowing trend in SS Spread will persist into the following week. More information is available in the "Differentials" section of www.mabux.com.

European natural gas prices have fallen to below €40 per megawatt-hour, marking the lowest point in the past two months. This drop can be attributed to persistently low demand, which has allowed the region to maintain robust gas reserves. Despite a recent cold spell, withdrawals from storage have been minimal compared to previous years. As of December 2nd, EU gas storage stands at 94.4%, slightly lower than the 97.7% reported a week ago. Germany's reserves have decreased to 95.2% (down from 99.2%), France at 94.6% (down from 98.7%), and Italy at 93.5% (down from 96.2%). In addition to these factors, temperatures are anticipated to rise by the end of the week, leading to a reduction in heating demand. Furthermore, a challenging economic outlook suggests limited potential for a significant increase in industrial consumption of natural gas in the near future.

The price of LNG as bunker fuel in the port of Sines (Portugal) experienced a significant drop, decreasing by 95 USD to reach 892 USD/MT on December 05. The price gap between LNG and traditional fuel also narrowed to 18 USD in favor of MGO, as compared to the 93 USD difference observed a week prior. On this day, MGO LS was quoted at 874 USD/MT in the port of Sines. More information is available in the LNG Bunkering section of www.mabux.com.

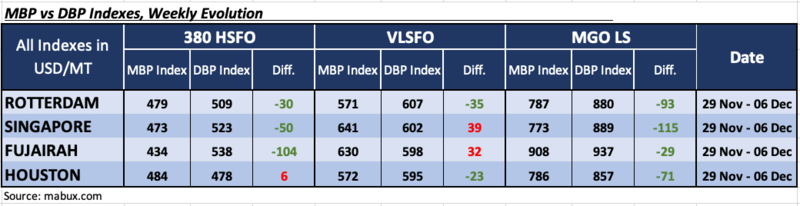

In the 49th week, the MDI index (the ratio of market bunker prices (MABUX MBP Index) vs. the MABUX digital bunker benchmark (MABUX DBP Index)) displayed the following trends in four selected ports: Rotterdam, Singapore, Fujairah and Houston:

In the 380 HSFO segment, Houston moved into the overcharge zone, with the overprice weekly average increasing by 18 points. The other three ports remained undervalued. The underprice weekly average fell by 2 points in Rotterdam and 11 points in Singapore. The MDI index in Fujairah remained unchanged at the end of the week, continuing to exceed the $100 mark.

In the VLSFO segment, according to the MDI, Singapore and Fujairah were in the overcharge zone, with the average weekly premium declining by 34 points in Singapore and 14 points in Fujairah. In Rotterdam and Houston, VLSFO remained undervalued. Weekly average levels of undercharging fell by 1 point in Rotterdam and 22 points in Houston.

In the MGO LS segment, all ports remained undervalued. The weekly average narrowed further by 2 points in Rotterdam, 9 points in Fujairah and 22 points in Houston. In Singapore, the weekly average consistently remaining above $100.underprice premium, on the contrary, widened by 5 points,

Overall, changes in the MDI index in the world's largest hubs during the week did not indicate the formation of a sustainable dynamics in the correlation of market prices and the digital benchmark.

More information on the correlation between market prices and the MABUX digital benchmark is available in the “Digital Bunker Prices” section of www.mabux.com.

The count of green-corridor initiatives aimed at facilitating zero-carbon shipping worldwide has more than doubled this year, surging from 21 at the close of 2022 to a current tally of 44. These initiatives advocate for the decarbonization of shipping by ensuring the availability of zero-carbon fuels along crucial trade routes. The driving forces behind these initiatives are heightened governmental commitments to establish green corridors and sustained efforts from the industry and ports. Among the 171 stakeholders actively engaged in green corridors, shipping companies, ports, and the third sector collectively constitute over half. Notably, 18 governments are directly involved, with 19 initiatives showcasing public or public-private leadership.

We expect the Global bunker indices may continue trending downwards in the upcoming week.

By Sergey Ivanov, Director, MABUX

All news