The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

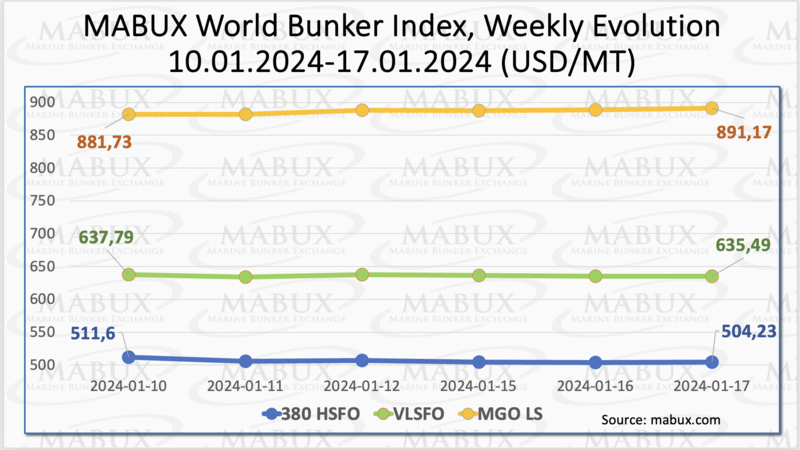

During Week 03, the MABUX global bunker indices displayed an inconsistent trend, fluctuating in various directions. The 380 HSFO index fell by 7.37 USD: from 511.60 USD/MT last week to 504.23 USD/MT. The VLSFO index, in turn, lost 2.30 USD (635.49 USD/MT versus 637.79 USD/MT last week). The MGO index, on the contrary, increased by 9.44 USD (from 881.73 USD/MT last week to 891.17 USD/MT). At the time of writing, a moderate downward trend prevailed in the Global bunker market.

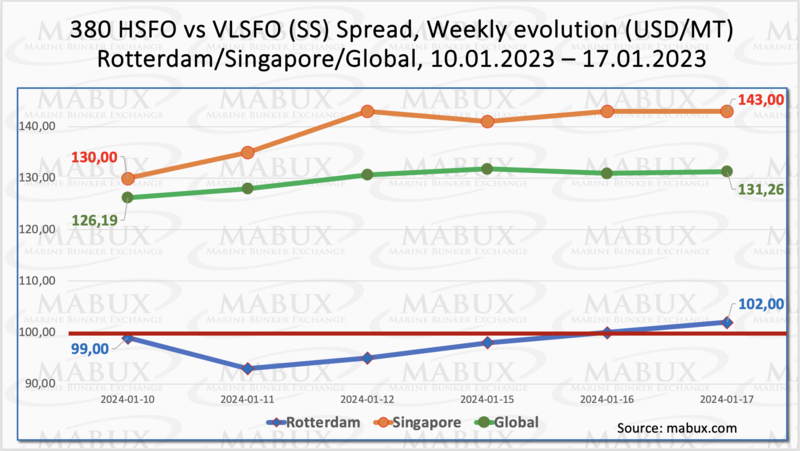

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - witnessed moderate growth, amounting to plus $5.07 ($131.26 versus $126.19.39 last week). The weekly average increased by $2.76. In Rotterdam, SS Spread rose by $3.00 (from $99.00 last week to 102.00), hovering close to the $100 mark, although the weekly average dropped by $10.00. In Singapore, the 380 HSFO/VLSFO price difference widened by $13 ($143.00 versus $130.00 last week), and the weekly average also increased by $8.67. It is anticipated that the current upward trend in SS Spread is unlikely to continue into the next week. More information is available in the “Differentials” section of mabux.com.

In early January, benchmark gas prices in Europe reached their lowest point since last August. Traders anticipate that the ample gas stored will meet demand until spring. Currently, European gas storage is at 83% capacity, a satisfactory level for this season. Despite this, European buyers are not solely relying on stored gas, as they continue to procure LNG, and the supply from the U.S. remains strong, making storage utilization during the winter months optional. Concurrently, gas demand has decreased significantly across most of Europe, primarily due to elevated prices and government policies.

The price of LNG as bunker fuel in the port of Sines (Portugal) continued its directed decline, reaching 674 USD/MT on January 15 (minus 66 USD compared to the previous week). Concurrently, the price difference between LNG and conventional fuel on January 15 favored LNG by 181 USD versus 92 USD a week earlier: MGO LS was quoted that day in the port of Sines at 855 USD/MT. More information is available in the LNG Bunkering section of www.mabux.com.

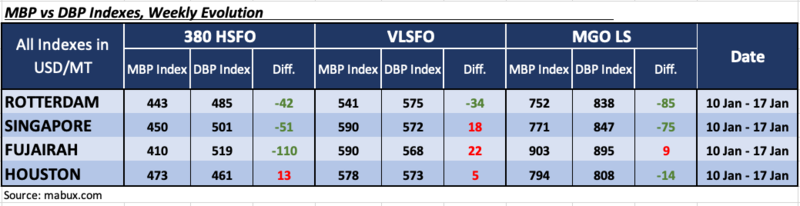

During the 03rd week, the MDI index (the ratio of market bunker prices (MABUX MBP Index) vs. the MABUX digital bunker benchmark (MABUX DBP Index)) revealed the following trends in four selected ports: Rotterdam, Singapore, Fujairah and Houston:

In the 380 HSFO segment, Houston remained the sole overvalued port, with the average weekly overpricing decreasing by 24 points. The remaining three ports were in the undercharge zone. The weekly average underpricing increased by 6 points in Rotterdam, 20 points in Singapore and 15 points in Fujairah, where the MDI index exceeded the $100 mark again.

In the VLSFO segment, according to MDI, Houston shifted to the overcharge zone, joining Singapore and Fujairah. The weekly average fell by 11 points in Singapore, 19 points in Fujairah, but rose by 8 points in Houston. The only undervalued port in this bunker fuel segment remains Rotterdam, where the weekly average increased by 16 points.

In the MGO LS segment, the only overpriced port is Fujairah, where the weekly average fell by 12 points. The remaining three selected ports were undervalued, with the average level of underpricing showing an increase of 17 points in Rotterdam, 5 points in Singapore and 1 point in Houston.

The dynamics of the MDI index in the world's largest hubs remain uncertain.

More information on the correlation between market prices and the MABUX digital benchmark is available in the “Digital Bunker Prices” section of www.mabux.com.

The most recent data from DNV reveals a notable surge in the adoption of alternative fuel propulsion, with 298 ships ordered in 2023, marking an 8% increase from the previous year. Methanol, in particular, experienced a significant uptick in interest, emerging as a mainstream choice with 138 orders – nearly quadrupling the 35 recorded in 2022. This positioned methanol on par with LNG, which garnered 130 orders. Container ships led the way as the primary adopters of methanol propulsion, accounting for 106 of the total orders, followed by bulk carriers (13) and car carriers (10). DNV also highlighted 2023 as a pivotal year for ammonia, with 11 orders for ammonia-fueled vessels and more in the pipeline. However, hydrogen faced a decline in popularity, with only five orders in 2023, compared to 18 in 2022. LNG orders experienced a decrease from 222 to 130 year-on-year, placing it behind methanol in terms of popularity. Nevertheless, LNG surpassed the 1,000-vessel milestone (excluding LNG carriers), underscoring its ongoing significance in the maritime energy transition. The container segment led LNG adoption with 48 vessels ordered, followed by car carriers (40) and tankers (30). Despite the dip in LNG orders, the overall landscape reflects the maritime industry's commitment to diverse and sustainable fuel options.

The recently released annual piracy report from the International Maritime Bureau (IMB) has underscored concerns stemming from the first successful Somali-based hijacking since 2017. The report reveals a year-on-year (y-o-y) escalation in reported maritime piracy and armed robbery incidents, rising from 115 in 2022 to 120 in the past year. These incidents comprised 105 vessel boardings, nine attempted attacks, four vessels hijacked, and two instances of vessels being fired upon. Of particular note, the Gulf of Guinea accounted for three out of the four globally reported hijackings, emphasizing its persistent status as perilous waters for seafarers.

We expect that the current escalation of tensions in the Middle East and the ongoing conflict in Ukraine could provoke an increase in global bunker prices next week.

By Sergey Ivanov, Director, MABUX

All news