The Bunker Outlook was contributed by Marine Bunker Exchange (MABUX)

During the 11th week, the MABUX global bunker indices showed a moderate decline. The 380 HSFO index fell by 2.43 USD: from 536.82 USD/MT last week to 534.39 USD/MT. Similarly, the VLSFO index decreased by 2.17 USD, reaching 676.01 USD/MT compared to 678.75 USD/MT the previous week. The MGO index lost 2.77 USD (from 896.98 USD/MT last week to 894.21 USD/MT), consistently below the 900 USD mark. At the time of writing, the market was in a moderate upward trend.

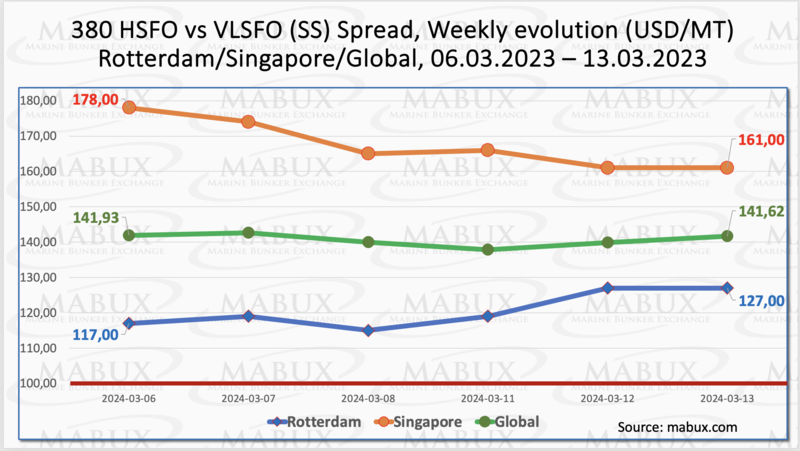

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - remained stable, decreasing by a nominal $0.31 ($141.62 versus $141.93 last week). The weekly average also saw a decrease of $8.05. In Rotterdam, SS Spread increased by $10.00, rising from $117.00 to 127.00, while the weekly average remained almost unchanged, with a slight increase of $0.84. Conversely, in Singapore, the 380 HSFO/VLSFO price difference narrowed by $17.00 ($161.00 versus last week's $178.00), and the weekly average dropped by $23.33. Overall, the SS Spread showed minimal fluctuations without a distinct trend, varying slightly in different directions. More information is available in the “Differentials” section of www.mabux.com.

Global spot gas prices have exhibited a downward trajectory, with European spot gas and Asian spot LNG prices decreasing from approximately USD 10 per million Btu at the end of 2023 to the USD 09 by the end of January and further declining to the USD 08 in late February 2024. This trend may enhance the demand for LNG cargoes, particularly in LNG markets across Asia, Africa, and South America.

The cost of LNG as bunker fuel at the port of Sines, Portugal, experienced a slight reduction, dropping to 634 USD/MT on March 11, marking a decrease of 1 USD compared to the previous week. The price disparity between LNG and traditional fuel also narrowed on March 11, with LNG holding an advantage of 221 USD, in contrast to the 277 USD difference observed a week earlier. On the mentioned date, MGO LS was priced at 885 USD/MT in the port of Sines. More information is available in the LNG Bunkering section of www.mabux.com.

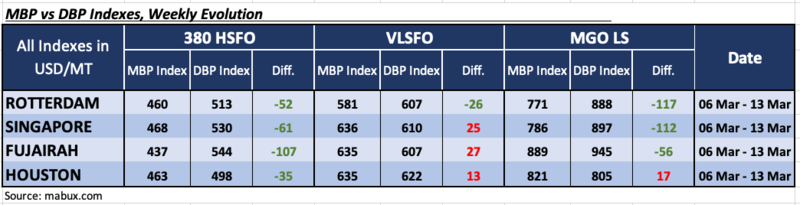

During Week 11, the MDI index (the ratio of market bunker prices (MABUX MBP Index) vs. the MABUX digital bunker benchmark (MABUX DBP Index)) recorded the following trends in four selected ports: Rotterdam, Singapore, Fujairah and Houston:

In the 380 HSFO segment, all four selected ports remained in the undercharge zone. The average weekly underprising fell by 5 points in Rotterdam, 22 points in Singapore, 12 points in Fujairah and 3 points in Houston. The MDI index in Fujairah remained above the $100 mark.

In the VLSFO segment, according to MDI, Rotterdam was the only undervalued port. The weekly average decreased by another 7 points. The remaining three selected ports were overestimated. Average weekly premium rose by 8 points in Fujairah and 7 points in Houston. The MDI index in Singapore remained unchanged.

As for the MGO LS segment, Houston remained the only overpriced port, with the average weekly margin decreasing by 3 points. The other three ports were underpriced, with the average weekly premium rising by 8 points in Rotterdam and 7 points in Singapore but falling by 3 points in Fujairah. The MDI index in Rotterdam and Singapore remained above the $100 mark.

The overall ratio of undervalued and overvalued ports in the 380 HSFO, VLSFO and MGO LS segments did not change during the week, while the MDI index did not show a sustained trend.

More information on the correlation between market prices and the MABUX digital benchmark is available in the “Digital Bunker Prices” section of www.mabux.com.

According to the recent DNV report, ten methanol-fueled vessels were ordered last month, bringing the total number of methanol-fueled ships, either in operation or on order, to 267. The majority of these orders pertain to containers (167), followed by bulk carriers (17) and oil/chemical tankers (15), with the latter having the highest number of methanol-fueled vessels currently in operation (25). In the LNG sector, the number of vessels in operation or on order increased from 1,016 in January to 1,033 in February. Notably, the number of LNG-fueled vessels in operation exceeded 500, reaching a total of 509. Among these, the container segment takes the lead with 191 vessels in operation, followed by crude oil tankers (77) and oil/chemical tankers as the next most popular segments. Despite having only 25 LNG-fueled vessels currently in operation, the car carrier segment has a substantial total of 154 vessels on order, making it the second-highest after the container segment, which has a total of 191. Additionally, last month witnessed the confirmation of an order for the world's first ammonia-powered container vessel, Yara Eyde.

We expect that the state of temporary stabilization in the global bunker market will persist. Bunker indices are expected to continue fluctuating in different directions.

By Sergey Ivanov, Director, MABUX

All news