The Bunker Review was contributed by Marine Bunker Exchange (MABUX)

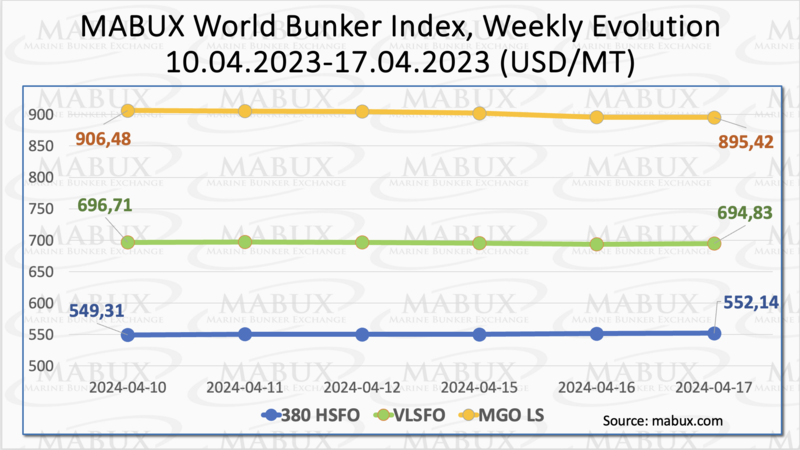

During Week 16, the MABUX global bunker indices showed mixed dynamics with no a clear trend. The 380 HSFO index rose by 2.83 USD: from 549.31 USD/MT last week to 552.14 USD/MT. The VLSFO index fell by 1.88 USD (694.83 USD/MT versus 696.71 USD/MT last week), consistently staying below the $700 mark. The MGO index decreased by 11.06 USD (from 906.48 USD/MT last week to 895.42 USD/MT), falling below the 900 USD mark. At the time of writing, there are signs of a downward trend in the global bunker market.

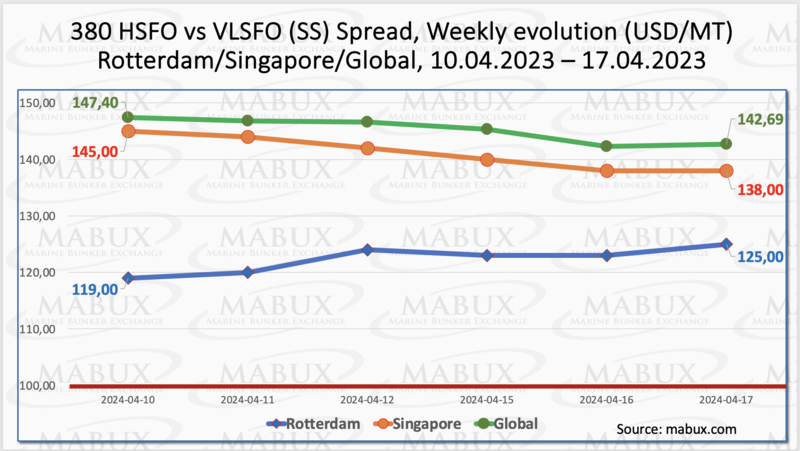

MABUX Global Scrubber Spread (SS) – the price difference between 380 HSFO and VLSFO - decreased by $4.71 ($142.59 vs. $147.40 last week). At the same time, the weekly average showed a symbolic decrease of $0.26. In Rotterdam, SS Spread increased by $6.00 (from $119.00 last week to 125.00), maintaining above the $100.00 mark (SS Breakeven), with the weekly average up by $4.50. Conversely, in Singapore, the difference in the price of 380 HSFO/VLSFO, reduced by $7.00 ($138.00 versus $145.00 last week), with the weekly average down by $1.66. We expect continued uncertainty in the SS Spread dynamics for the upcoming week. More information is available in the "Differentials" section of mabux.com.

European natural gas prices surged last week due to Russia's escalation of attacks on Ukrainian energy infrastructure. This retaliation followed a series of Ukrainian strikes on Russian oil refineries. Reuters estimates that these attacks have disrupted approximately 14% of Russia's total refining capacity. Washington has criticized these energy-focused attacks, expressing concerns that they could further elevate global oil prices. Additionally impacting European natural gas futures were reports of significantly reduced natural gas flows into the Freeport LNG export plant in Texas, attributed to problems with a liquefaction train.

On April 15, the price of LNG as bunker fuel in the port of Sines, Portugal, rose to 730 USD/MT, marking an increase of 89 USD from the previous week. Concurrently, the price gap between LNG and conventional fuel narrowed to 165 USD in favor of LNG, down from 285 USD the previous week. On the same day, MGO LS was priced at 895 USD/MT in the port of Sines. For further details, refer to the LNG Bunkering section on www.mabux.com.

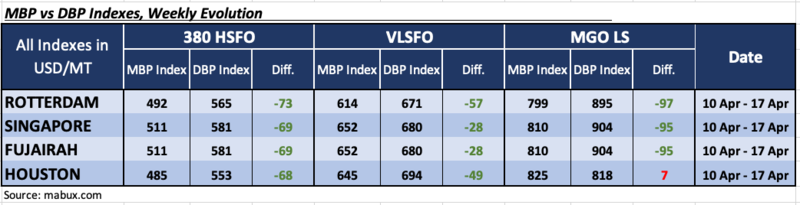

In Week 16, the MDI index (the ratio of market bunker prices (MABUX MBP Index) vs. MABUX digital bunker benchmark (MABUX DBP Index)) highlighted the following trends across the major world hubs: Rotterdam, Singapore, Fujairah and Houston:

In the 380 HSFO segment, all selected ports registered undercharging. Weekly averages rose by 7 points in Rotterdam and Houston, while decreasing by 4 points in Singapore and a significant 41 points in Fujairah, where the MDI index dropped below the $100 mark.

In the VLSFO segment, all ports remained undervalued according to the MDI. Weekly averages rose by 1 point in Rotterdam and 8 points in Houston but declined by 1 point in Singapore and 5 points in Fujairah.

In the MGO LS segment, Houston shifted to the overcharge zone, with the average weekly ratio increasing by 8 points. All other ports remained undervalued, with weekly levels declining by 21 points in Rotterdam and 25 points in Singapore. In Fujairah, the underprice rate rose by 17 points. Both Rotterdam and Singapore MDI indices fell below the $100 mark.

By week's end, the balance between overvalued and undervalued ports in the 380 HSFO and VLSFO segments remained unchanged, while in the MGO LS segment, Houston emerged as the sole overpriced port amid overall undervaluation. We foresee minimal shifts in the MDI port index next week, with the prevailing trend of fuel underestimation persisting.

More information on the correlation between market prices and the MABUX digital benchmark is available in the “Digital Bunker Prices” section of www.mabux.com.

Danish Shipping has announced its intention to comply with a ban on scrubber water discharge and has urged for strict enforcement. Following an agreement reached by a wide political consensus, ships navigating through Danish waters will no longer be permitted to discharge exhaust gas system wash water. This ban on scrubber water discharge will be enforced within Denmark's territorial sea, extending up to 12 nautical miles (approximately 22 km) from the coastline. The agreement also commits Denmark to advocate for similar bans in the Baltic Sea and North Sea through regional sea conventions HELCOM and OSPAR. The ban will be implemented in two phases: from 1 July 2025, for ships using scrubbers in open operation that discharge wash water directly into the sea, and from 1 July 2029, for ships employing scrubbers in closed operation.

The Panama Canal Authority anticipates a return to normal transit capacity by next year, following a period of reduced capacity due to low water levels. This decrease in transits has been notable after Panama recorded its third-driest year on record in 2023. According to the authority, the canal has averaged 27 transits per day this year, a decline from the usual 36 transits per day during the rainy season.

Next week, we anticipate continued market volatility with irregular shifts in bunker indices.

By Sergey Ivanov, Director, MABUX