The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

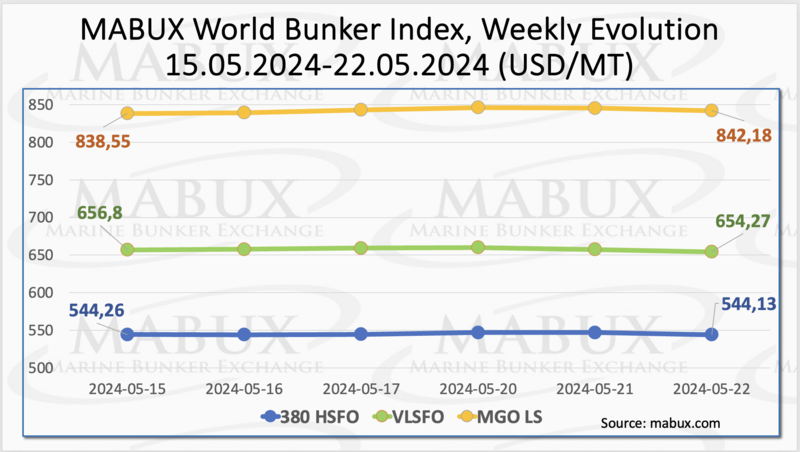

In Week 21, the MABUX global bunker indices showed irregular changes with no clear trend. The 380 HSFO index decreased by a symbolic 0.13 USD: from 544.26 USD/MT last week to 544.13 USD/MT. The VLSFO index fell by 2.53 USD (654.27 USD/MT versus 656.80 USD/MT last week). The MGO index, on the contrary, increased by 3.63 USD (from 838.55 USD/MT last week to 842.18 USD/MT). At the time of writing, a steady downward trend was observed in the global bunker market.

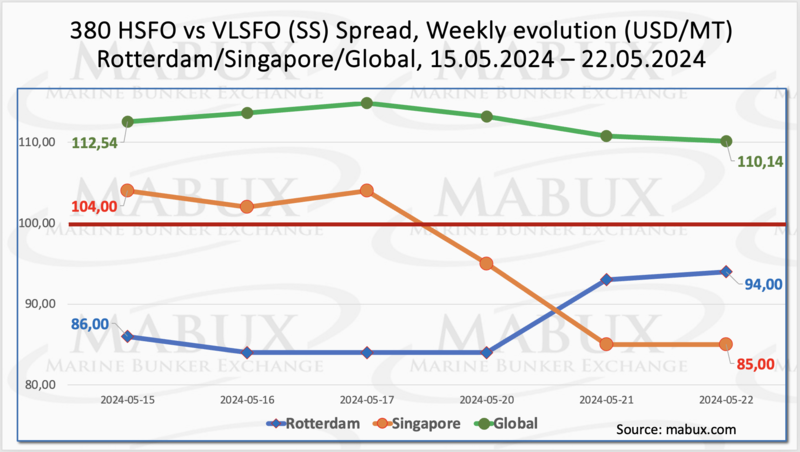

The MABUX Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - returned to a moderate decline: minus $2.40 ($110.14 versus $112.56 last week), gradually approaching the $100.00 mark (SS Breakeven). The weekly average also fell by $0.95. In Rotterdam, SS Spread, on the contrary, showed growth: plus $8.00 (from $86.00 last week to 94.00), also gradually rising to the $100.00 mark. The port's weekly average rose by $1.17. In Singapore, the 380 HSFO/VLSFO price differential narrowed unexpectedly to minus $19.00 ($85.00 versus last week's $104.00), falling below $100, with the weekly average down $5.67. Thus, the dynamics of the SS Spread still lack pronounced dynamics. In the near future, we expect a further reduction in SS Spread to levels below $100 SS Breakeven. More information is available in the "Differentials" section of www.mabux.com.

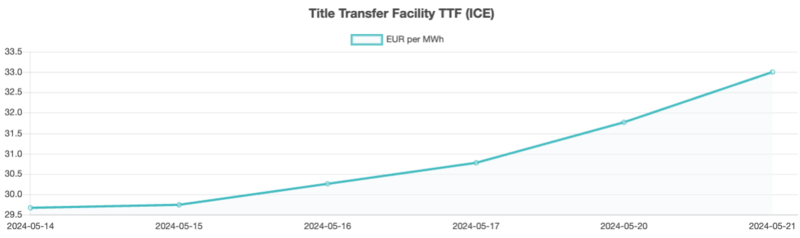

In April 2024, worldwide LNG imports reached a record high of 34.52 million metric tons (Mt), marking a 1.7% increase (0.58 Mt) year-on-year. The Asia Pacific and LAC regions spearheaded this surge, compensating for a significant downturn in European LNG imports. From January to April 2024, global LNG imports grew by 2.9% (3.98 Mt) year-on-year, totaling 142.52 Mt. During Week 21, the European gas benchmark TTF continued its moderate growth, adding 3.335 EUR/MWh (33.004 EUR/MWh versus 29.669 EUR/MWh last week).

The price of LNG as bunker fuel in the port of Sines (Portugal) continued its upward trend, reaching 728 USD/MT on May 20, an increase of 32 USD compared to last week. Simultaneously, the price difference between LNG and conventional fuel on May 20 decreased to 89 USD in favor of LNG, down from 117 USD the previous week. On that day, MGO LS was quoted in the port of Sines at 817 USD/MT. More information is available in the LNG Bunkering section of www.mabux.com.

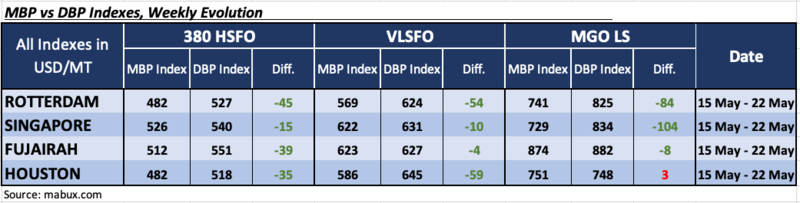

In Week 21, the MDI index (the correlation ratio of market bunker prices (MABUX MBP Index) vs. MABUX digital bunker benchmark (MABUX DBP Index)) registered the following trends across the major world hubs: Rotterdam, Singapore, Fujairah and Houston:

In the 380 HSFO segment, all selected ports were in the undercharge zone. Weekly averages fell 3 points in Singapore and 2 points in Fujairah but rose 5 points in Houston. The MDI index in Rotterdam remained changed.

In the VLSFO segment, according to the MDI, all ports remained undervalued, with average weekly levels showing an increase of 4 points in Singapore and 3 points in Houston, and a decrease of 2 points in Rotterdam and 1 point in Fujairah. Fujairah's indices remained at 100 percent correlation between the market price and the MABUX digital benchmark.

In the MGO LS segment, Houston was the only overvalued port, with the weekly average rising 2 points, while the index remained near the 100 percent correlation mark between market price and the MABUX digital benchmark. All other ports were undervalued. Average weekly margins showed a further 6-point decline in Rotterdam, but an increase of 5 points in Singapore and 2 points in Fujairah. The MDI index in Singapore exceeded the $100 mark again.

At the end of the week, the balance of overvalued/undervalued ports in all market segments did not change, while underpricing remained the prevailing trend.

For more details on the correlation between market prices and the MABUX digital benchmark, visit the “Digital Bunker Prices” section on www.mabux.com.

JLC reported, that in April, Chinese refiners produced approximately 1.2 million metric tons (mt) of Very Low Sulfur Fuel Oil (VLSFO), a decrease from the 1.4 million mt produced in March. This represents a 9% decline in the daily average VLSFO output, down to 41,000 mt/day. The reduction in VLSFO production is attributed to increased seasonal maintenance activities at refineries. Consequently, this has led to a constrained supply of VLSFO for bunkering in Zhoushan, a major Chinese port, with suppliers suggesting lead times of 5-7 days due to the lower output and limited barge availability. To support future VLSFO production, the Chinese government has issued 4 million mt in export quotas for bonded bunkering, as part of the second allocation round for the year. These new export quotas are anticipated to enhance VLSFO output later in the year.

We expect downward trend to prevail in the global bunker market next week.

By Sergey Ivanov, Director, MABUX

All news