The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

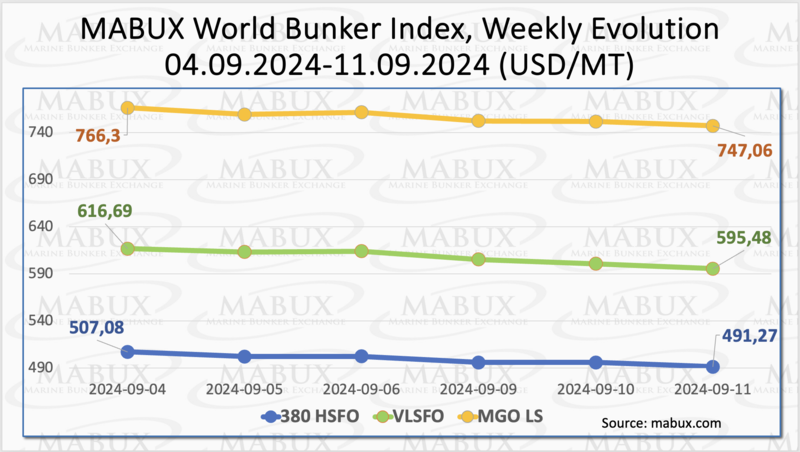

In Week 37, the MABUX global bunker indices continued their downward trend for the second consecutive week. The 380 HSFO index fell by USD 15.81, from USD 507.08/MT last week to USD 491.27/MT, breaking through the USD 500 mark. The VLSFO index dropped by USD 21.21, declining from USD 616.69/MT to USD 595.48/MT, moving below the USD 600 level. Meanwhile, the MGO index decreased by USD 19.24, from USD 766.30/MT to USD 747.06/MT. At the time of writing, an upward correction was observed in the global bunker market.

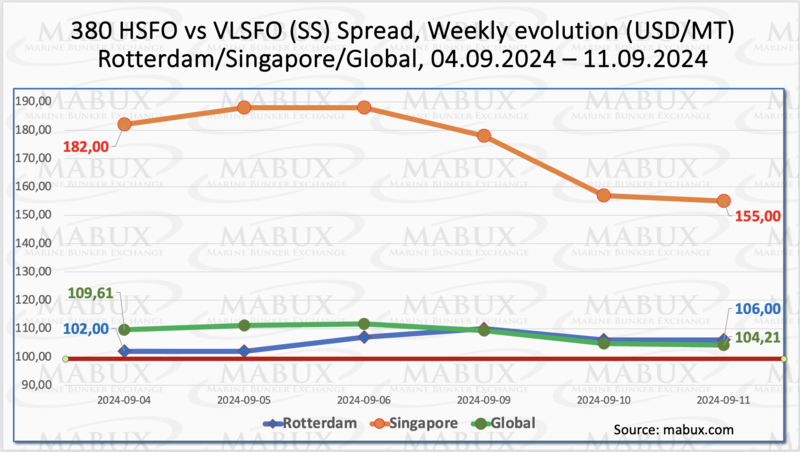

The MABUX Global Scrubber Spread (SS) – the price difference between 380 HSFO and VLSFO – narrowed by $5.51, from $109.61 to $104.21, nearing the SS breakeven point of $100.00. The weekly average, however, increased by $1.02. In Rotterdam, the SS Spread rose by $4.00, maintaining its position above the $100.00 level, with $106.00 compared to $102.00 last week. The weekly average widened by $6.50. In Singapore, the 380 HSFO/VLSFO price spread shrank sharply by $27.00, falling from $182.00 to $155.00, while the weekly average in the port increased by $7.50. The upward dynamics of the SS Spread appear to have lost momentum, with global and port-specific indices showing mixed changes, which are expected to continue next week. Detailed information can be found in the "Differentials" section on www.mabux.com.

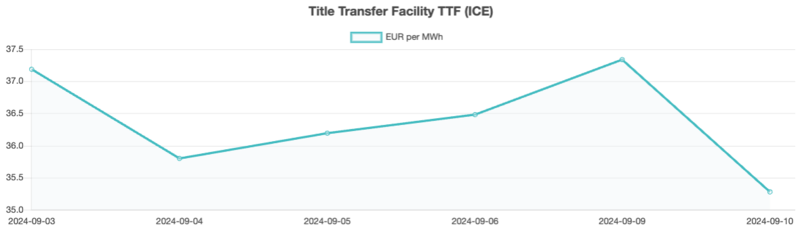

As of September 10, European regional storage facilities were 93.09% full. By the end of Week 37, the European gas benchmark TTF declined by 1.911 EUR/MWh, from 37.193 EUR/MWh to 35.282 EUR/MWh.

By the end of the week, the price of LNG as bunker fuel in the port of Sines (Portugal) had dropped by $14, reaching $849/MT on September 09. Meanwhile, the price gap between LNG and conventional fuel continued to widen on September 9, MGO LS was priced $128 lower than LNG, compared to a $112 difference the previous week. MGO LS was quoted at $721/MT in the port of Sines on that day. More detailed information is available in the LNG Bunkering section on www.mabux.com.

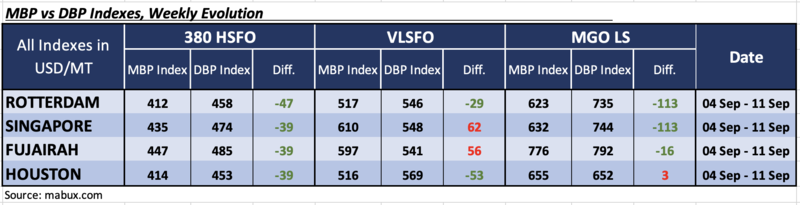

For Week 37, the MDI index (the correlation ratio of market bunker prices (MABUX MBP Index) vs. MABUX digital bunker benchmark (MABUX DBP Index)) indicated the following trends across the four largest global hubs: Rotterdam, Singapore, Fujairah and Houston:

• 380 HSFO segment: All four ports were undervalued. Weekly averages rose by 4 bps in Rotterdam, but fell by 7 bps in Singapore, 29 bps in Fujairah, and 7 bps in Houston.

• VLSFO segment: Singapore and Fujairah remained in the overvalued zone, with weekly averages rising by 25 bps and 30 bps respectively. Rotterdam and Houston continued to be undervalued. Weekly averages fell by 9 bps in Rotterdam and 8 bps in Houston.

• MGO LS segment: Houston moved into the overvalued zone, becoming the only overpriced port, with its weekly average increasing by 6 bps. The other three ports were undervalued. The underpricing average decreased by 3 bps in Rotterdam, 2 bps in Singapore, and 33 bps in Fujairah. The MDI indices in Rotterdam and Singapore remained stable above the $100 mark.

By the end of the week, the balance of overvalued/undervalued ports shifted slightly toward overvaluation, although the general trend of underpricing continues to dominate the global bunker market.

For more details on the correlation between market prices and the MABUX digital benchmark, visit the “Digital Bunker Prices” section on www.mabux.com.

ClassNK forecasts that peak demand for LNG and methanol as marine fuels could reach 24 million tonnes and 4.5 million tonnes, respectively, by 2026. This growth is attributed to the large-scale delivery of LNG-fueled vessels, comparable to the current fleet size, and the steady addition of methanol-fueled vessels, especially container ships currently on order. For liquefied petroleum gas (LPG), ClassNK noted that gas carriers are the only vessel type expected to use the fuel, with peak demand forecasted at one million tonnes by 2026. The classification society also highlighted that while current demand for ammonia and hydrogen remains limited, it is expected to grow as vessels powered by these fuels are introduced. The updated report also tracks trends in vessel types using alternative fuels. According to ClassNK, there are 53 bulk carriers, 106 container ships, 60 crude tankers, 70 product/chemical tankers, six gas carriers, and 31 road carriers capable of running on LNG. The methanol-fueled fleet consists of seven container ships and 25 product/chemical tankers. Additionally, six LNG-fueled LPG carriers and 127 LPG tankers are capable of running on LPG.

We expect the global bunker market will experience moderate, irregular fluctuations next week, with no clear trend emerging.

By Sergey Ivanov, Director, MABUX

All news