The Bunker Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

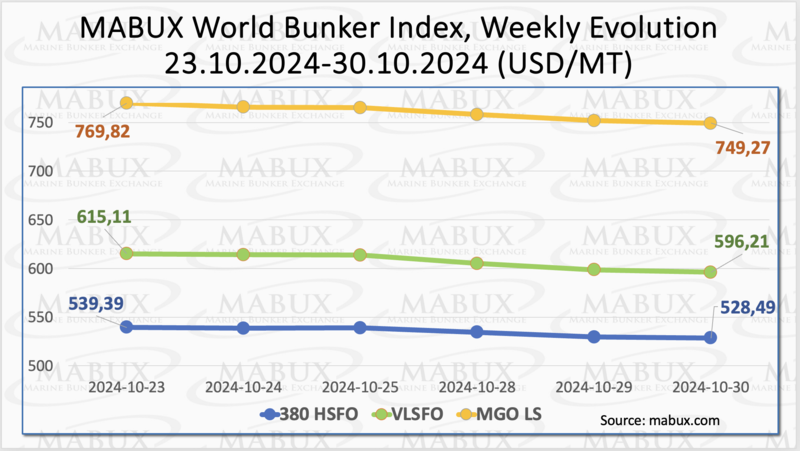

In Week 44, the MABUX global bunker indices exhibited a general decline. The 380 HSFO index fell by USD 10.90: from USD 539.39/MT last week to USD 528.49/MT. The VLSFO index decreased by USD 18.90 (USD 596.21/MT versus USD 615.11/MT last week), crossing below the USD 600.00 mark. The MGO index declined by USD 20.55 (from USD 769.82/MT last week to USD 749.50/MT). At the time of writing, the global bunker indices were experiencing a moderate upward correction.

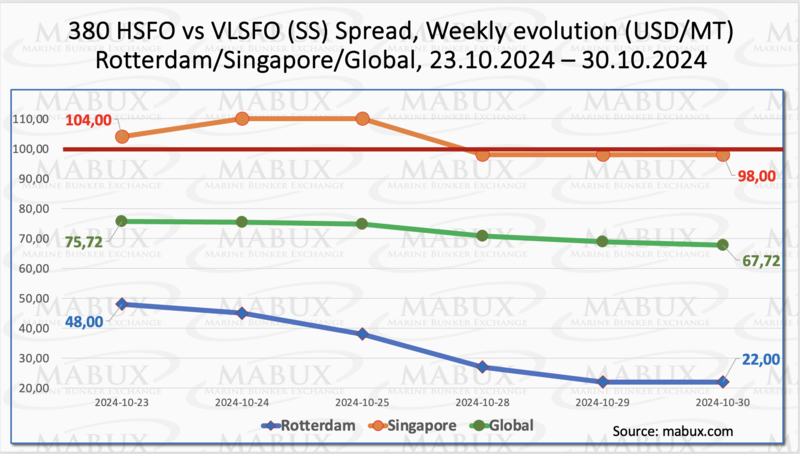

MABUX Global Scrubber Spread (SS) - the price differential between 380 HSFO and VLSFO - continued to narrow, decreasing by another $8.00 (from $75.72 last week to $67.72), and remaining well below the $100.00 mark (SS Breakeven). The weekly average also dropped by $6.26. In Rotterdam, SS Spread saw a sharp contraction, dropping by USD 26.00 to USD 22.00 from USD 48.00 last week, marking the lowest point since the IMO 2020 regulations took effect on January 1, 2020. The weekly average there also decreased by $25.66. In Singapore, the 380 HSFO/VLSFO price differential narrowed by $6.00: from $104.00 last week to $98.00, breaking the $100.00 mark. The weekly average in the port decreased by $8.33. The reduction in SS Spread is impacting the economic viability of the 380 HSFO + scrubber option. We anticipate this narrowing trend between 380 HSFO and VLSFO to continue next week. Further information is available in the Differentials section of www.mabux.com.

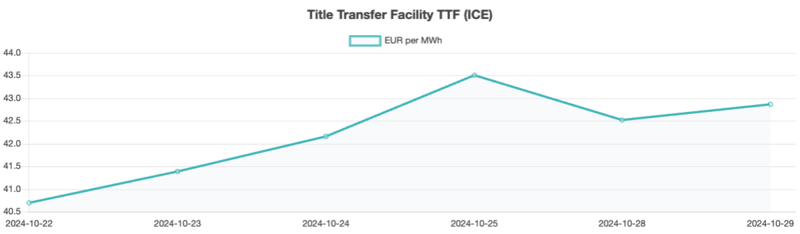

Europe’s natural gas prices rose through the second and third quarters of 2024 but remained marginally lower and significantly less volatile than in 2023. Increased Norwegian supply availability, a robust storage position, and subdued European demand offset pressures from a tighter global LNG market driven by rising global gas demand and geopolitical tensions. As of October 28, European regional storage facilities were 95.32% full, following the bloc's early achievement of its 90% storage target in August, well ahead of the November 1 deadline. By the end of week 44, the European gas benchmark TTF had risen by €2.165/MWh (€42.869/MWh vs. €40.704/MWh last week).

The price of LNG as a bunker fuel in the port of Sines (Portugal) spiked by USD 81 last week, reaching USD 948/MT on October 29. Meantime, the price gap between LNG and conventional fuel on October 29 widened significantly again: MGO LS was priced at USD 719/MT, making it USD 229 cheaper than LNG, compared to a USD 154 difference the previous week. More detailed information is available in the LNG Bunkering section of www.mabux.com.

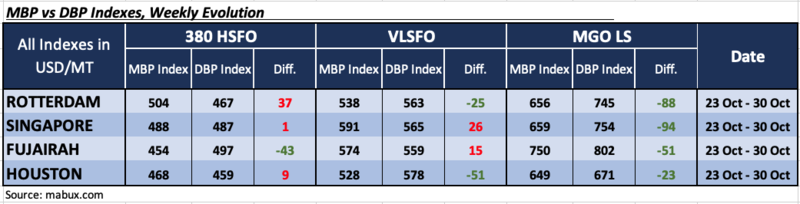

During Week 44, the MDI index (the correlation ratio of market bunker prices (MABUX MBP Index) vs. MABUX digital bunker benchmark (MABUX DBP Index) registered the following trends across the four largest global hubs: Rotterdam, Singapore, Fujairah and Houston:

• 380 HSFO segment: Singapore and Houston moved into the overcharge zone, joining Rotterdam. The weekly overprice average rose by 17 points in Rotterdam, 10 points in Singapore, and 12 points in Houston. The MDI index in Singapore is close to 100% correlation mark between the market price and the MABUX digital benchmark. Fujairah remained the only undervalued port in this bunker segment, while weekly average drop of 9 points.

• VLSFO segment: Singapore and Fujairah continued to be in overcharge zone, and the weekly averages rose by 3 points in Singapore but fell by 2 points in Fujairah. Rotterdam and Houston remained undervalued. The weekly averages rose by 8 and 2 points respectively.

• MGO LS segment: All four selected ports stayed in the undercharge zone. Weekly averages showed a further 6-point decline in Rotterdam and 1-point decline in Singapore, but a 3-point gain in Fujairah and a 9-point gain in Houston.

Over the week, the balance of overvalued/undervalued ports had completely moved into the undervalued zone. The trend towards undervaluation of all types of bunker fuel remains dominant in the global bunker market.

At the end of the week, the balance of overvalued/undervalued ports shifted towards overvalued ports in the 380 HSFO segment. However, the overall trend of undervaluation remains dominant. More insights are available in the “Digital Bunker Prices” section at www.mabux.com.

The Port of Rotterdam reported a total throughput of 328.6 million tonnes for the first three quarters of this year, a slight 0.4% decrease compared to 2023. Container throughput was the strongest performer in Q3, with a 3% year-on-year increase by weight to 101.1 million tonnes, attributed to rising consumer spending in Europe. However, liquid bulk throughput declined by 1.7% in the first nine months, including a 3.6% drop in crude oil, caused by unexpected maintenance at a German refinery and low refinery margins. LNG throughput fell slightly below last year's figure of 300,000 tonnes, as high natural gas reserves in Europe reduced demand. Additionally, LNG spot cargoes were increasingly redirected to Asia, where prices are slightly higher. The report also noted a significant drop in biofuels throughput. In summary, the Port Authority stated that rising consumer confidence led to growth in container throughput. However, the decline in other segments reflects the ongoing challenges faced by European industry, which continues to struggle with weak competitiveness due to high energy costs.

Despite this week’s drop in bunker prices, we expect that an upward correction will prevail in the global bunker market next week.

By Sergey Ivanov, Director, MABUX

All news