The Weekly Outlook was contributed by Marine Bunker Exchange (MABUX)

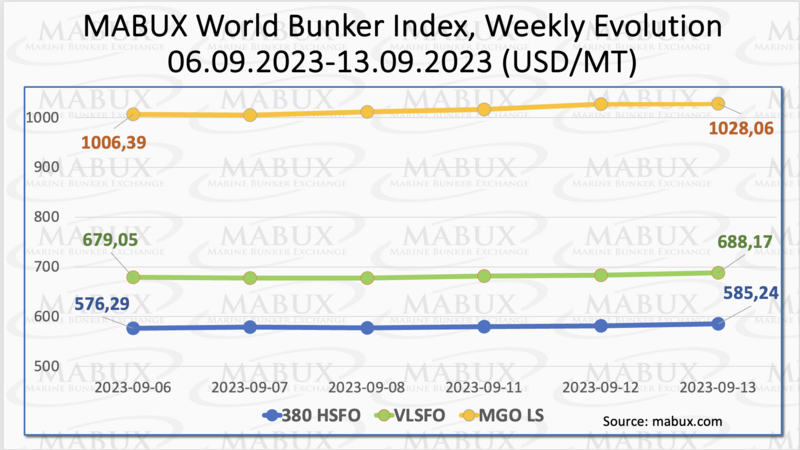

Over the Week 37, the MABUX global bunker indices continued upward trend. The 380 HSFO index rose by 8.95 USD, climbing from 576.29 USD/MT last week to 585.24 USD/MT. The VLSFO index, in turn, increased by 9.12 USD (688.17 USD/MT versus 679.05 USD/MT last week). The MGO index surged even more significantly: plus 21.67 USD (from 1006.39 USD/MT last week to 1028.06 USD/MT), confidently surpassing the 1000 USD mark. At the time of writing, bunker indices continued trending upwards.

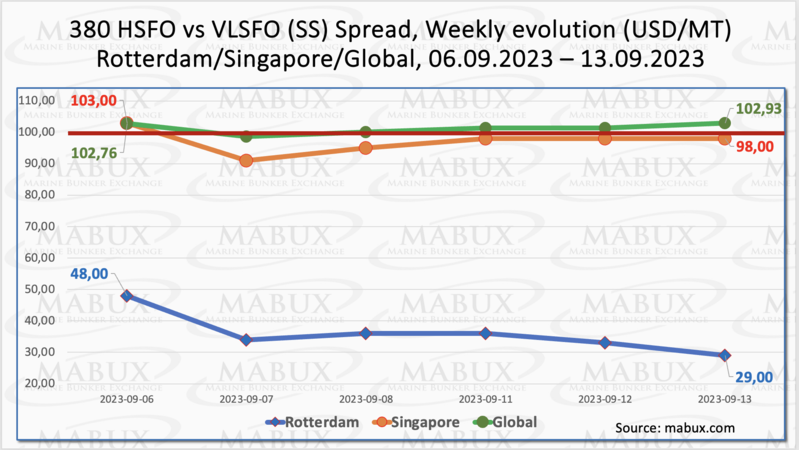

Global Scrubber Spread (SS) - the price difference between 380 HSFO and VLSFO - remained largely stable, adding a marginal $0.17 and reaching $102.93 compared to $102.76 from the previous week, still in proximity to the $100.00 mark (SS breakeven point). Meantime, the weekly average showed a slight increase of $0.41. In Rotterdam, SS Spread continued its decline, losing another $19.00, from $48.00 last week to $29.00. This marks the lowest value for SS Spread in Rotterdam since April 27, 2020. The weekly average SS Spread in Rotterdam also fell by $12.33. In Singapore, the difference in the price of 380 HSFO/VLSFO over the week also decreased by $5.00 ($98.00 versus $103.00 last week), breaking through the $100 mark. The weekly average decreased by $10.66. Given the current dynamics, it is expected that the SS Spread may continue to contract next week. More information is available in the “Differentials” section of www.mabux.com.

Following the uptrend in gas indications, the price of LNG as bunker fuel in the port of Sines (Portugal) increased, reaching 840 USD/MT on September 12 (plus 82 USD compared to the previous week). At the same time, the difference in price between LNG and conventional fuel remained virtually unchanged on September 12: 214 USD in favor of LNG versus 220 USD a week earlier: MGO LS was quoted that day in the port of Sines at 1054 USD/MT. More information is available in the LNG Bunkering section of www.mabux.com.

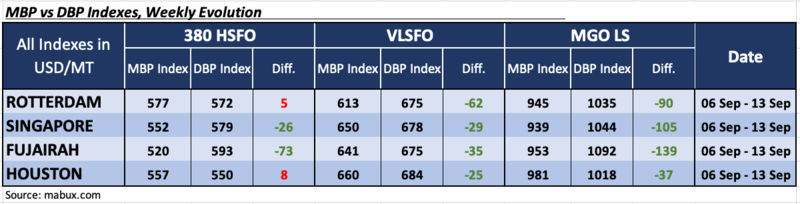

During Week 37, the trend of the MDI index (the ratio of market bunker prices (MABUX MBP Index) and the digital bunker benchmark MABUX (MABUX DBP Index) remained unchanged: the majority of selected ports were underpriced for all types of bunker fuel.

In the 380 HSFO segment, Singapore and Fujairah continued to be undervalued, with the average weekly underpricing remaining unchanged in Singapore and increasing by 8 points in Fujairah. Conversely, in the other two ports, Rotterdam and Houston, the MDI index indicated a slight overpricing, with a weekly average decrease of 2 points in Rotterdam and 12 points in Houston.

In the VLSFO segment, according to MDI, all four selected ports were undervalued. The average undercharge index rose by 13 points in Rotterdam, 13 points in Singapore, 9 points in Fujairah and 13 points in Houston.

In the MGO LS segment, all selected ports remained underpriced, with the average undervaluation showing a significant increase: 25 points in Rotterdam, 26 points in Singapore, 29 points in Fujairah, and 16 points in Houston.

Hence, the trend of undervaluation in the global bunker fuel market persists. More information on the correlation between market prices and the MABUX digital benchmark is available in the “Digital Bunker Prices” section of www.mabux.com.

In the latest update of its Maritime Forecast up to 2050, DNV has issued a warning regarding the shipping industry's imperative to explore alternative strategies for emissions reduction. This is driven by fierce competition from other transportation sectors and industries for the supply of carbon-neutral fuels. The classification society has also emphasized that the maritime sector's ability to meet its 2030 emission reduction targets is hanging in the balance. DNV emphasizes the need for a flexible approach, with a focus on enhancing energy efficiency alongside adopting new fuels. DNV's calculations indicate that to meet the projected demand of 17 million tonnes of oil equivalent (Mtoe) annually by 2030, the maritime industry will have to secure a substantial share, amounting to an astonishing 30-40%, of the global carbon-neutral fuel supply.

When discussing promising energy efficiency measures, such as air lubrication systems and wind-assisted propulsion, DNV highlights that wind-assisted propulsion has already demonstrated its effectiveness. It has been implemented on 28 large vessels, resulting in fuel savings ranging from 5-9%, with the potential for even greater efficiency gains. In addition to wind-assisted propulsion, nuclear propulsion has established itself as a viable option in the naval sector, boasting an installed base of approximately 160 vessels. In summary, although progress has been made, only 6.5% of the current ship tonnage operates on alternative fuels, compared to 5.5% in the previous year. This indicates that a significant majority, 93.5% of the global fleet by tonnage, continues to rely on conventional fuels.

We expect the upward trend in the global bunker market to continue next week.

By Sergey Ivanov, Director, MABUX